Tesla Deep Dive

The Architect of Abundance: Why Tesla isn’t a Car Company

In early April 2026, Elon Musk took one of the boldest steps yet in his decades-long quest to reshape humanity’s future: SpaceX confidentially filed for what could become the largest initial public offering in history, with a targeted valuation approaching $2 trillion.

If successful, this IPO would mint him as the world’s first trillionaire and mark a pivotal moment where his seemingly separate empires begin to converge. Insiders and observers, including biographer Walter Isaacson, have noted it could be a steppingstone toward deeper integration between SpaceX’s orbital capabilities, xAI’s advancements, and Tesla’s autonomous systems and humanoid robotics.

The same visionary who once bet everything on reusable rockets that most experts dismissed as fantasy is now positioning his companies to potentially combine forces, leveraging Starship’s heavy-lift power, vast satellite networks, and cutting-edge AI to supercharge Tesla’s robotaxis, Optimus humanoid robots, and energy ambitions. Just months earlier, Musk had declared 2026 would be “epic” and “amazing” for Tesla, even as the company quietly retooled factories away from legacy models to prioritize AI-driven autonomy and robotics.

Science fiction is quickly becoming reality. This is Musk’s engineering reality at warp speed, turning what skeptics call overpromising into a multi-planetary, AI-augmented industrial machine. And at the center of it all sits Tesla: no longer “just a car company,” but the earthly proving ground for the physical AI and sustainable abundance he envisions.

Before diving into Tesla, it is necessary to understand Musk’s philosophy on understanding the universe and the meaning of life, which he answers in the below 3-minute interview clip.

Executive Summary

The Mission: A Civilizational Mandate

Tesla’s mission is not merely to sell cars, but to accelerate the world’s transition to sustainable energy. Unlike competitors who view EVs as a regulatory requirement or a market segment, Musk views the transition as a civilizational imperative to prevent “the end of the world as we know it.” Every product, from the Model Y to the Megapack, is a tactical step toward solving the carbon equation.

Gannon Capital Internal Thoughts: I have to call this out right away, because it remains one of the greatest misconceptions in the investment world: Tesla should not be valued or analyzed primarily as a traditional automobile company. Sure, it still designs and sells highly desirable electric vehicles that generate the bulk of its revenue today but treating it as “just a car company” is like calling Apple “just an iPod company” on the eve of the iPhone launch. The vehicles, and rapidly-growing energy business, have served as the essential cash engine and data platform to fuel the real endgame: full self-driving autonomy, robotaxis, and humanoid robotics via Optimus. Tesla’s own recent moves, retooling factories away from legacy models toward AI and robots, make this strategic shift unmistakable.

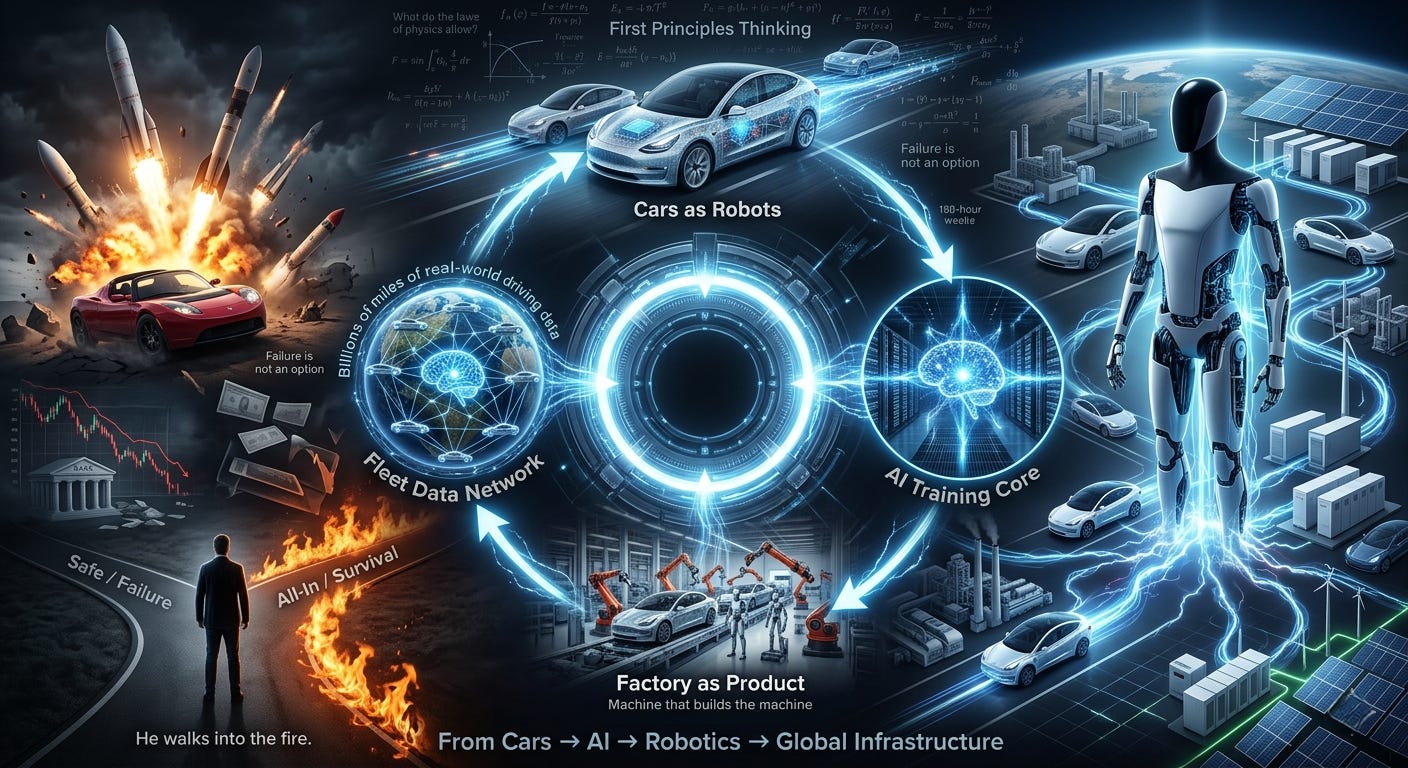

The AI & Robotics Feedback Loop

Tesla is a vertically integrated robotics and AI firm disguised as an automaker.

The Car as a Robot: Tesla’s vehicles are sophisticated edge-computing devices.

The Factory as a Product: Tesla views high-volume manufacturing, the “Machine that builds the machine” as its true competitive advantage.

The Data Moat: By using its fleet as a massive, distributed sensor network, Tesla captures real-world driving data that legacy Original Equipment Manufacturers OEMs and Waymo cannot match, creating an insurmountable lead in AI-driven autonomy.

The Elon Difference: First Principles and Radical Risk

What differentiates Elon Musk from the global cohort of CEOs is a combination of First Principles Thinking and an extraordinary threshold for pain.

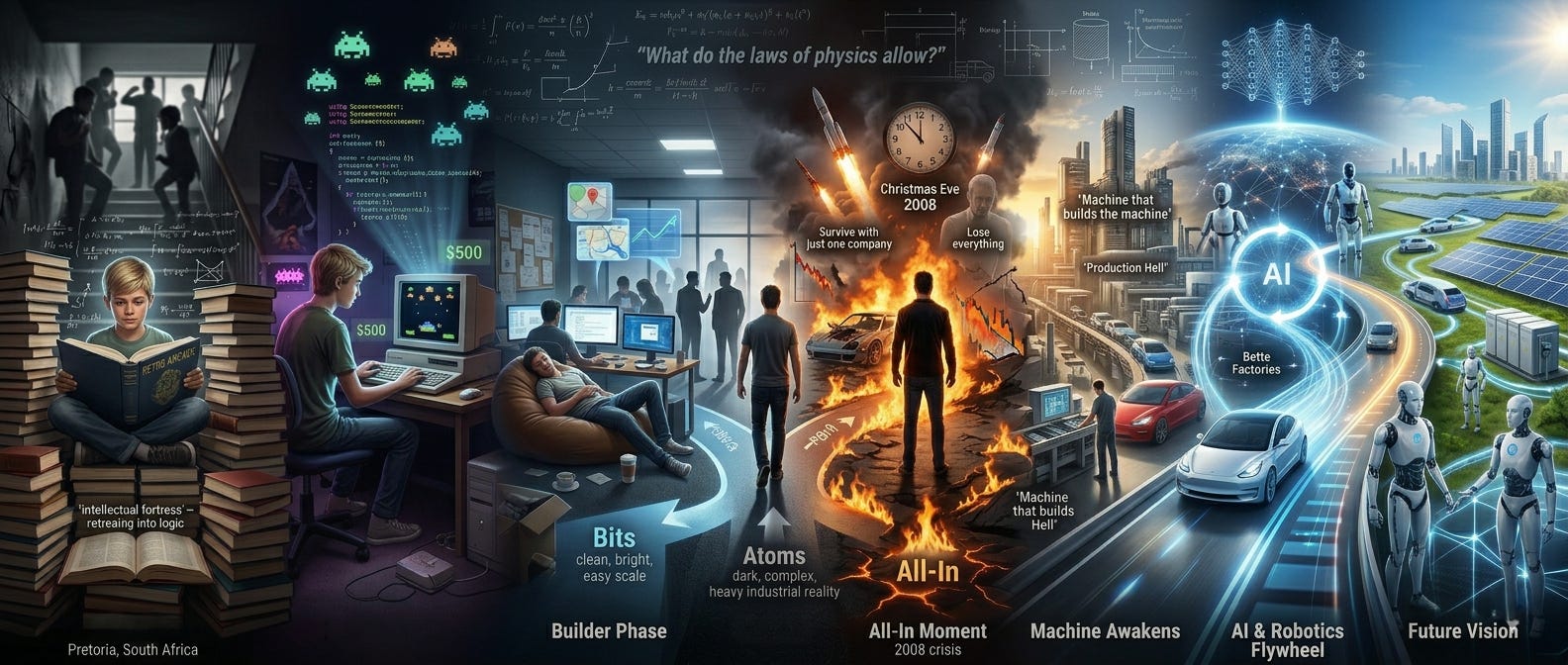

Engineering Depth: As Ashlee Vance notes in his biography, Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic Future, Musk is not a “suits and ties” CEO; he is a Chief Engineer who understands the physics of a battery cell as well as the economics of the supply chain. He doesn’t ask “what does the industry do?” but “what do the laws of physics allow?”

The Absence of a Safety Net: Musk’s career is defined by “betting the farm.” In 2008, he poured his last $40 million, the entirety of his PayPal fortune, into Tesla and SpaceX while living on personal loans from friends. He does not hedge; he chooses the path of maximum consequence.

Demon Mode: Vance describes Musk’s ability to enter a state of hardcore intensity where failure is treated as a physical impossibility. This culture has been imprinted on Tesla, creating an organization that thrives in “production hell” where others would collapse.

Failure is Not an Option: The 2008 Crucible

The defining moment of Tesla’s origin was the 2008 financial crisis. With the Roadster failing to launch on time and SpaceX’s first three rockets exploding, Musk faced total ruin.

The Choice: He could have split his remaining cash between the two companies (likely killing both) or focused on one. Instead, he chose to go all-in on both, working 120-hour weeks (17-hour days, seven days a week).

The Result: His refusal to accept a controlled bankruptcy forced the hand of investors and partners. This “burn the boats” strategy is the DNA of Tesla; the company operates with a permanent sense of urgency because Musk views every delay as a threat to the mission.

Shaping the World: The “Tesla Effect”

Musk’s vision has fundamentally reordered the global economy:

Forcing the Pivot: Before the Model S, the world’s largest automakers (Toyota, VW, GM) dismissed EVs as “compliance cars.” Musk proved that an EV could be better, faster, and cooler than an internal combustion engine car, forcing the entire $2.5 trillion global auto industry to pivot.

Energy Sovereignty: By scaling the Powerwall and Megapack, Musk is decentralizing the energy grid, moving the world toward a future where “the sun and the wind” are the primary fuels for humanity.

The Standard Bearer: From the North American Charging Standard (NACS) to the use of large-scale casting, Tesla’s innovations are now the blueprints for the rest of the industrial world.

The Core Question

Can Tesla successfully transition from being the world’s leading EV manufacturer to a high-margin software, AI, and robotics powerhouse? The valuation of the company rests on whether Musk can once again defy the laws of business to solve Full Self-Driving (FSD) and scale Optimus, effectively turning Tesla into the world’s most valuable AI enterprise.

The Origin Story: The Making of a Magnate

To understand Tesla, one must first understand the psychological architecture of its founder. Elon Musk did not emerge from the traditional corridors of the American automotive industry; he was forged in a crucible of social isolation, intellectual obsession, and a traumatic childhood in apartheid-era South Africa. As Ashlee Vance chronicles, the Elon Musk the world sees today is a man who learned early on that the world is a place to be conquered, not merely inhabited.

Pretoria and the Survival Mindset

The Intellectual Fortress:

In the isolation of his youth in Pretoria, South Africa, Musk developed an obsessive relationship with information, famously consuming two entire sets of encyclopedias before his tenth birthday.

This was a psychological defense mechanism for a child who struggled with social cues, the objective laws of physics and history provided a stable reality that people did not.

The Crucible of Bullying:

Vance details the horrific incident where Musk was hunted by a group of boys, thrown down concrete stairs, and beaten until he was unrecognizable.

This trauma did not break him; it calloused him. It instilled a survival mindset where pain became a secondary concern to the mission at hand.

This period explains the hardcore culture at Tesla today. If Musk could survive the literal threat of death as a child, he views “production hell” as a manageable challenge.

The Blastar Era: Logic as a Weapon

The Digital Epiphany:

At age 12, Musk wrote the code for Blastar, a space-invader style game, and sold the source code for $500. The game is still playable today.

This was his first proof of concept that a lone individual, armed with a computer, could create value and influence the world from a bedroom.

The Birth of First Principles Thinking:

Musk realized that the physical world, like software, is governed by a set of “base code” or “the laws of physics.”

He began to reject reasoning by analogy, doing things because that’s how they’ve been done, in favor of breaking problems down to their fundamental truths and rebuilding from there.

The Zip2 and X.com Lessons: Monastic Devotion

The Ethics of Intensity:

During the Zip2 years, Musk lived a life of monastic discipline. He rented no apartment, instead sleeping on a beanbag in the office and showering at the YMCA to maximize coding time.

Fun fact: In the early 1990s, while a student at Queen’s University in Canada (and later at UPenn), Musk wanted to see if he could survive on $1 a day for food. He bought food in bulk, primarily eating hot dogs, oranges, pasta, and the occasional green pepper. Musk did this to prove to himself that he could survive on very little money. He believed that if he could live on $1 a day, he wouldn’t need a high salary and could take significant risks to start his own technology companies. He later stated that this experience gave him the mental freedom to pursue big goals, as he knew he could handle financial hardship.

He demanded his employees match his 100-hour work weeks, establishing the asymmetric effort philosophy that defines Tesla’s engineering pace.

Zip2, later X.com, provided the seed capital and the battle scars that allowed Musk to create the company that eventually merged with Cofinity to become PayPal.

The PayPal War Chest:

Following the $1.5 billion acquisition of PayPal by eBay, Musk walked away with roughly $180 million when he was 31.

Musk viewed this capital as fuel. To him, money was never the end state; it was the necessary resource to fund his master plan for humanity.

The “PayPal Mafia” Divergence: While Musk’s associates, including Peter Thiel (Facebook/Palantir), Reid Hoffman (LinkedIn), and the YouTube founders (Chen, Hurley, and Karim) reinvested their millions into high-margin, low-CAPEX software “bits,” Musk took the unique and perilous path of betting his entire $180M fortune on “atoms,” funding the massive physical infrastructure and heavy manufacturing required to bring Tesla and SpaceX to life.

Entering Tesla: From Investor to Architect

The Meeting of Minds:

In 2004, Martin Eberhard and Marc Tarpenning approached Musk with the idea for an electric sports car.

Musk saw the venture not as a car company, but as a way to solve the “Carbon Equation.” He led the Series A with $6.5 million, effectively becoming the company’s primary benefactor.

The Boardroom Coup:

Musk’s involvement was never meant to be passive. He obsessed over every detail, from the door latches to the carbon fiber body of the Roadster.

As costs spiraled, Musk realized that for the mission to succeed, he had to take total control. He ousted Eberhard and assumed the CEO role, signaling the shift from a niche startup to a relentless, Musk-led machine.

The “Near Death” Experience (2008)

The Convergence of Ruin:

By late 2008, Musk was fighting a two-front war. Three SpaceX rockets had exploded, and Tesla was weeks away from running out of cash.

The global financial crisis had frozen the credit markets, and no one was interested in funding a high-risk electric car startup.

The 11th Hour Bet:

Musk faced a choice: split his remaining millions between the two companies and likely see both die, or choose one to have a better shot at surviving.

True to his Failure is Not an Option mindset, he chose a third option: he went all-in on both, bluffing his investors by claiming he would personally fund the round to force their hand.

The deal closed on Christmas Eve 2008. Tesla was saved with hours to spare.

The Psychological Legacy:

This near-death moment is the most important chapter in Tesla’s history. It created a company that operates with a permanent sense of existential urgency.

Musk learned that he could survive total public humiliation and financial ruin, which rendered him effectively fearless in the face of future impossible odds.

The Product Ecosystem: More Than Just a Car

The Master Plan (Parts 1, 2, and 3): The Strategic Roadmap

Part 1 (The Luxury-to-Mass Pivot): Published in 2006, this was Musk’s blueprint for disrupting the status quo: build a high-performance sports car (Roadster) to prove EVs were desirable, use that money to build a luxury sedan (Model S), and finally use those profits to fund a high-volume, affordable car (Model 3).

Part 2 (The Autonomy and Integration Pivot): Released in 2016, this shifted the focus to solar roof integration, a broader vehicle lineup (trucks and buses), and the transition from cars you drive to autonomous fleets that earn you money while you sleep.

Part 3 (The Global Scale Pivot): Unveiled in 2023, this plan addresses the End Game: scaling battery production to 240 TWh to transition the entire global economy to sustainable energy, including planes, boats, and industrial heating.

Hardware: Reimagining the Machine

The S3XY Lineup (The Core Fleet):

Tesla’s Model S, 3, X, and Y represent a masterclass in platform standardization. By sharing parts and software across models, Tesla achieved manufacturing efficiencies that legacy automakers, burdened by hundreds of different engine configurations, simply could not match.

Fun Fact: The Model 3 was meant to be the Model E, but Ford held the trademark for the name and threatened to sue Tesla, famously prompting Musk to remark that “Ford is killing sex” before he pivoted to the “3” (a stylized “E”) to maintain the “S3XY” model lineup acronym.

Cybertruck (The Manufacturing Radical):

The Cybertruck is a case study in first principles material science. By using an Ultra-Hard Cold-Rolled stainless-steel exoskeleton instead of a traditional frame, Tesla eliminated the need for expensive paint shops and stamping dies, effectively reinventing how a vehicle is structured.

Software & AI: The Digital Nervous System

The First-Mover Data Moat:

While competitors like Waymo rely on expensive LiDAR and pre-mapped HD maps, Musk made the “bet-the-company” decision to use Vision Only (cameras and Neural Nets).

The Logic: Humans drive using vision and biological neural nets; therefore, a machine should do the same. This allows Tesla to scale autonomy anywhere in the world without needing specialized infrastructure or expensive hardware sensors.

Dojo (The AI Engine):

To process the billions of miles of video data collected by the Tesla fleet, the company built Dojo, a custom-designed supercomputer.

Dojo represents Tesla’s transition into a high-margin Compute-as-a-Service provider, potentially rivaling NVIDIA in specialized AI training efficiency.

Optimus (The Humanoid Endgame):

Tesla’s humanoid robot is not a side project; it is the ultimate application of Tesla’s technology stack (batteries, actuators, and computer vision).

Musk views Optimus as a solution to the global labor shortage and the product that could eventually make Tesla the most valuable company in the world by decoupling economic output from human labor.

Energy: The “Stepchild” and Future Giant

The Megapack (Utility Scale):

Tesla’s massive container-sized batteries are designed to stabilize the global electric grid. As coal and gas plants retire, Megapacks provide the buffer needed for intermittent wind and solar power.

The Powerwall (Residential Sovereignty):

By combining solar with home storage, Tesla is effectively turning houses into micro-utilities, allowing consumers to disconnect from a failing or expensive traditional grid; and in some cases, even sell the additional power back to the grid resulting in a credit on the electric bill.

Growth Velocity:

In recent quarters, Tesla’s Energy segment has begun growing at a significantly faster percentage rate than its Automotive segment. Musk’s long-term vision is for Tesla Energy to be as large as, or larger than, the car business, reflecting the total addressable market (TAM) of the entire global energy grid.

The Business Model & Competitive Moats

The First-Mover Data Moat:

By being the first to market with high-performance, long-range EVs, Tesla has successfully captured market share (about 50% of the USA as of April 2026) while deploying a global sensor network.

While legacy automakers treat a car sale as a final transaction, Tesla treats every vehicle as a distributed data collector. With over 5 million connected cars on the road, Tesla captures billions of miles of real-world edge cases, unusual driving scenarios, that cannot be simulated in a lab.

This creates an insurmountable lead in AI: while competitors like Waymo test with hundreds of cars, Tesla uses its entire customer fleet to train its Full Self-Driving (FSD) neural networks in shadow mode, refining the software against human behavior in real-time.

The Trojan Horse Strategy: From Hardware Flood to Software Yield

Flooding the Zone: Tesla’s strategy over the last decade has been to flood the global market with millions of connected hardware devices (the fleet). While legacy automakers view a car sale as the end of the revenue relationship, Tesla views it as the deployment of a dormant revenue-generating node.

The Switch to Autonomy: With the transition to unsupervised FSD in 2026, these millions of hardware devices are being fundamentally reclassified. They are no longer just depreciating personal vehicles; they are becoming revenue-generating robots.

The Shared Economy of Abundance: This creates a unique dual-incentive model:

For the Owner: The vehicle transitions from a cost center to a cash-flow asset. Through the Tesla Network, an owner can opt-in their car to the Robotaxi fleet while they sleep or work, earning passive income that could theoretically offset the entire monthly payment of the car.

For Tesla: This represents the ultimate high-margin pivot. Tesla will likely take a platform fee, similar to Apple’s 30% App Store cut, for every autonomous mile driven. This allows Tesla to scale a global transportation network without the massive overhead of owning the fleet themselves, effectively crowdsourcing the world’s largest autonomous taxi company using their customers’ capital.

The Financial Endgame: By flooding the market with hardware first, Tesla has built an insurmountable installed base. A software update can now turn on billions of dollars in recurring, high-margin revenue overnight, a feat that no competitor can match because they lack the millions of vision-capable devices already on the road.

Vertical Integration: The First Principles Supply Chain:

Musk’s refusal to rely on traditional Tier-1 suppliers (like Bosch or Continental) allows Tesla to capture the margins that usually leak out of the automotive value chain.

The Seat and the Chip: Tesla famously builds its own seats and designs its own FSD Computer chips. This saves on cost and makes the company nimbler. If a part needs to change, Tesla iterates in days, while legacy OEMs must wait for a supplier’s three-year product cycle.

4680 Cells: By moving into battery manufacturing, Tesla is attempting to solve the ultimate bottleneck of the green transition. Controlling the chemistry and the form factor of the battery gives them a fundamental cost-per-kilowatt advantage that dictates the price of the final vehicle.

Direct-to-Consumer (DTC): Deleting the Middleman:

Tesla is the only major American automaker that does not use a third-party dealership network. This allows them to capture the 10% margin typically taken by dealers and ensures a unified, high-tech brand experience.

Software Relationship: Because Tesla owns the relationship with the customer, they can push Over-the-Air (OTA) updates that improve the car overnight. This turns a depreciating physical asset into an appreciating software asset, a concept that legacy dealers who profit from service and repairs, are incentivized to resist.

The Supercharger Network: The Strategic Toll Bridge:

Early on, Musk realized that “Range Anxiety” was the primary barrier to EV adoption. He spent billions building a proprietary, seamless charging infrastructure while others waited for the government to act.

The NACS Standard: In a stunning strategic victory, nearly every major automaker (Ford, GM, Rivian, etc.) has now adopted the North American Charging Standard (NACS). This transforms Tesla’s charging network from a walled garden into a universal utility, where every non-Tesla EV on the road eventually becomes a paying customer of Tesla’s energy ecosystem.

Manufacturing as a Product: The “Machine that builds the Machine”:

Musk’s greatest moat is his obsession with the factory floor. He views the assembly line as a product that can be optimized just like software code.

Giga-Casting: By using massive “Giga Press” machines to cast the front and rear of the car as single pieces of aluminum, Tesla eliminated hundreds of parts and thousands of welds. This significantly reduces CAPEX, factory footprint, and weight.

The “Unboxed” Process: Tesla’s next-gen manufacturing involves working on different sections of the car simultaneously in separate sub-assemblies before snapping them together at the end. This is designed to reduce the production cost by 50%, making the $25,000 EV a mathematical reality rather than a marketing hope.

The Terafactory Leap (Scaling the Mission):

While the industry was still struggling to comprehend the Gigafactory (producing Gigawatt-hours of batteries), Musk moved the goalposts to the Terafactory, a facility designed to produce Terawatt-hours (TWh) a unit of energy equivalent to one trillion watt-hours of battery capacity and millions of vehicles annually under a single roof.

To put the magnitude of this scale into perspective: If a single Terafactory produced one Terawatt-hour of battery capacity, that volume of energy storage is equivalent to the amount of electricity needed to power roughly 32% of the entire world for an hour. To put it another way, one Terawatt of constant power running for a year would satisfy 32% of all the world’s annual electricity needs.

By consolidating the entire supply chain, from raw lithium processing to final vehicle assembly, into a massive, vertically integrated “Tera” footprint, like Giga Texas, Tesla drastically reduces the logistics nightmare of moving parts across the globe, creating a cost-structure that competitors cannot replicate without starting from scratch.

Industry Analysis & TAM

The Global Transition: From Combustion to Electrons

The Regulatory Tailwind: The push for “Net Zero” by 2050 has become a structural mandate for global economies. With the EU and several U.S. states banning the sale of new ICE vehicles by 2035, the end of the internal combustion engine is a scheduled event for some of the world’s largest economies.

The Economic Inevitability: Beyond regulation, the transition is driven by the declining cost-curve of batteries. As EVs reach price parity with gas cars and eventually become cheaper to manufacture due to fewer moving parts, the shift becomes an economic certainty rather than a policy choice.

The China Threat: The Rise of Vertical Titans

BYD (Vertical Dominance & Volume): Tesla’s most formidable rival is no longer the legacy OEMs of the West, but BYD in Shenzhen. BYD is the ultimate vertically integrated competitor, manufacturing its own battery cells, the “Blade Battery”, and controlling its own microchips. By dominating the sub-$20,000 market with models like the Seagull, BYD has proved that it can out-pace Tesla in sheer mass-market volume, forcing Tesla to innovate on the “Unboxed” manufacturing process to maintain its low-cost edge.

Xiaomi (Smartphone-on-Wheels): Xiaomi represents a radical new breed of competitor that moves at the speed of consumer electronics rather than automotive cycles. By treating the vehicle as a mobile software platform first and a transportation device second, Xiaomi is leveraging its existing ecosystem of millions of users to create a seamless “Human x Car x Home” experience, challenging Tesla’s software supremacy in the world’s largest EV market.

The Geopolitical Tightrope: The Giga Shanghai Paradox

The Strategic Asset: Giga Shanghai is the “Crown Jewel” of Tesla’s global manufacturing, responsible for over 50% of total vehicle production and maintaining the company’s highest operational efficiencies. It serves as the essential export hub for Europe and the APAC region.

The Strategic Hostage: This reliance creates a unique sovereign risk. As US-China trade tensions escalate in 2026, Tesla is walking an unprecedented tightrope. Any significant disruption to the Shanghai supply chain, or a move by Beijing to favor national champions over foreign firms, represents a catastrophic risk to Tesla’s global volume. Tesla’s aggressive move into Giga Texas (Cortex) and the planned Terafactory footprint in North America is, in many ways, a massive hedge against this geopolitical exposure.

Legacy OEMs: The Innovator’s Dilemma and Stranded Assets

The Profitability Gap: Ford, GM, and VW remain trapped by the “Innovator’s Dilemma.” To fund their EV transitions, they must continue to sell profitable Internal Combustion Engine (ICE) vehicles, but every ICE sale further delays the scale needed to make EVs profitable.

The Software Chasm: Legacy manufacturers struggle with “spaghetti code” cars built from hundreds of different components with disparate software systems. They cannot easily transition to the “Single Central Nervous System” architecture that Tesla has mastered, leaving them years behind in the race for high-margin, software-defined autonomy. While legacy OEMs focus on surviving the decade, Tesla is focused on the next century.

Total Addressable Market (TAM): The Multi-Trillion Dollar Shift

From $2T to $10T+: Tesla’s TAM is evolving from the global automotive sales market to the combined markets of transportation-as-a-service and global energy.

The “Robotaxi” Multiplier: If Tesla solves Level 5 autonomy, the business shifts from selling a physical asset to selling a high-margin utility. The TAM for autonomous ride-hailing is estimated to be significantly larger than the car market itself, as it replaces the cost of human labor and private car ownership.

The Energy Sovereign: As the world moves toward wind and solar, the energy storage TAM becomes massive. Tesla’s Megapack business aims to provide the foundational infrastructure for the global electric grid, a market that is essentially as large as the global economy itself.

Robotics as a Service (RaaS): The Optimus Wildcard

The End of Labor Constraints: The TAM for the Optimus humanoid robot is theoretically infinite, as it targets the entire global labor market.

The Thesis: If a robot can perform any task a human can, moving boxes, assembling parts, or cleaning homes, the cost of labor drops to the cost of electricity.

The Product Shift: Musk views Optimus as the ultimate culmination of Tesla’s manufacturing and AI expertise. If successful, Tesla transitions from a transportation company to a general-purpose labor provider, a move that could decouple economic growth from human population constraints and redefine the valuation of the firm entirely.

Management, Culture, and the “Elon Risk”

The Ousting of the Originator: The Eberhard Conflict

In the early days of Tesla, Martin Eberhard was the CEO and public face of the company. However, as the development of the original Roadster spiraled into massive cost overruns and technical delays, Musk’s First Principles standards were violated.

Musk discovered that the actual cost to build the Roadster was nearly double what Eberhard had reported to the board. Viewing this as a failure of both engineering and integrity, Musk orchestrated a boardroom coup in 2007.

This moment defined the Tesla management style: there is no room for “good enough.” If a founder or executive cannot meet the physics-based reality of the timeline, they are removed. Musk then took over as CEO and seized the soul of the company to ensure it met his personal threshold for excellence.

The SolarCity Gambit: Bailout or Blueprint?

The 2016 Integration: In a move that nearly broke his relationship with Wall Street, Musk orchestrated Tesla’s $2.6 billion acquisition of SolarCity, a struggling solar installer founded by his cousins, Lyndon and Peter Rive.

The Skeptic’s View: Critics and short sellers viewed the deal as a “incestuous bailout” of a failing company, leading to a high-profile shareholder lawsuit that followed Musk for years.

The Master Plan Logic: For Musk, the acquisition was a first principles necessity. He argued that you cannot have a sustainable transport company without controlling the source of the electrons. By merging SolarCity into Tesla, he transformed a car company into a vertically integrated energy titan, laying the groundwork for the current record-breaking growth in the Tesla Energy segment.

The Insight: This deal highlights a recurring theme in the Musk empire, as he views his companies (Tesla, SpaceX, xAI) as a single, coherent machine. What look like reckless side-bets to the market are, in his view, the essential components of a unified life support system for humanity.

Gannon Capital Internal Thoughts: The Ultimate ROI on a Boys’ Weekend

I have to highlight the origin story of SolarCity because it’s a masterclass in how Musk’s leisure time often results in industrial-scale disruption. In 2004, Elon and his cousins, Lyndon and Peter Rive, were crammed into a motorhome driving across the Nevada desert toward Burning Man. While most people use that trip to disconnect from reality, Musk used the drive to convince his cousins that they needed to “look into solar” to save humanity.

By the time they reached Black Rock City, the blueprint for what would become the largest residential solar provider in the U.S. was already taking shape. It’s a legendary case for the “boys’ weekend”, while most groups come back with nothing but a hangover, STDs, and stories they can’t tell their wives, this group came back with a plan to decentralize the American energy grid.

From an investment perspective, this tells you everything you need to know about the Musk ecosystem: there is no “off” switch. For Elon, a road trip isn’t just a vacation; it’s a mobile think-tank. The acquisition of SolarCity years later wasn’t just a financial maneuver; it was the closing of a loop that began in a dusty RV two decades ago. If your boys’ weekend doesn’t result in a multi-billion-dollar vertical integration strategy, are you even trying?

The “Hardcore” Culture: Survival of the Aligned

Musk’s management style is famously binary: you are either all-in on the mission, or you are an obstacle. This has created the hardcore environment characterized by extreme work hours, rapid-fire iteration, and high turnover.

While traditional corporate cultures prioritize employee retention and work-life balance, Tesla prioritizes mission-velocity.

The Result: A self-selecting workforce. Those who remain at Tesla are often the highest-performing engineers in the world, driven not by a paycheck, but by the belief that they are working on the most important problems that exist in the world today.

Engineering First: The Death of the MBA

Unlike legacy automakers led by finance executives and MBAs, Tesla’s organizational chart is aggressively flat and dominated by engineers.

Musk famously despises process for the sake of process. At Tesla, any employee is encouraged to email the CEO directly if it solves a problem faster.

By removing the layers of middle management that plague companies like GM or Ford, Tesla can move from a design concept to a production-ready part in weeks rather than years. At Tesla, the Chief Engineer (Musk) is also the CEO, ensuring that technical reality always trumps financial convenience.

Key Person Risk: The Musk Premium vs. The Musk Discount

Tesla’s valuation is inextricably linked to Elon Musk. This creates a unique key person risk where his divided attention, running Tesla, SpaceX, X (formerly Twitter), xAI, and Neuralink, can lead to volatility in the stock price.

The Compensation Debate: The massive $56 billion pay package, and the subsequent legal battles, highlights the tension: Is Musk an employee to be managed, or a sovereign architect whose presence is the only thing standing between Tesla and becoming “just another car company?”

Investors must weigh the “Musk Premium” (his ability to achieve the impossible) against the “Musk Discount” (the risk of his brand becoming polarized or his attention being spread too thin).

The Ultimate End-State: A Multi-Planetary Species

To understand why Musk pushes Tesla so hard, one must look beyond Earth. In his view, Tesla and SpaceX are two halves of the same coin: The survival of human consciousness.

Tesla’s work in high-density batteries, autonomous robotics (Optimus), and localized solar energy isn’t just for suburban driveways; it is the foundational technology stack required to build a self-sustaining city on Mars.

Musk views Tesla as the “Life Support System” for the future of humanity. Every dollar of profit and every breakthrough in manufacturing is ultimately a contribution to the “Mars Fund”, the quest to ensure that humanity becomes a multi-planet species before we face a planetary catastrophe.

Financials & Key Metrics

Revenue Mix: The Divergence of Hardware and Services

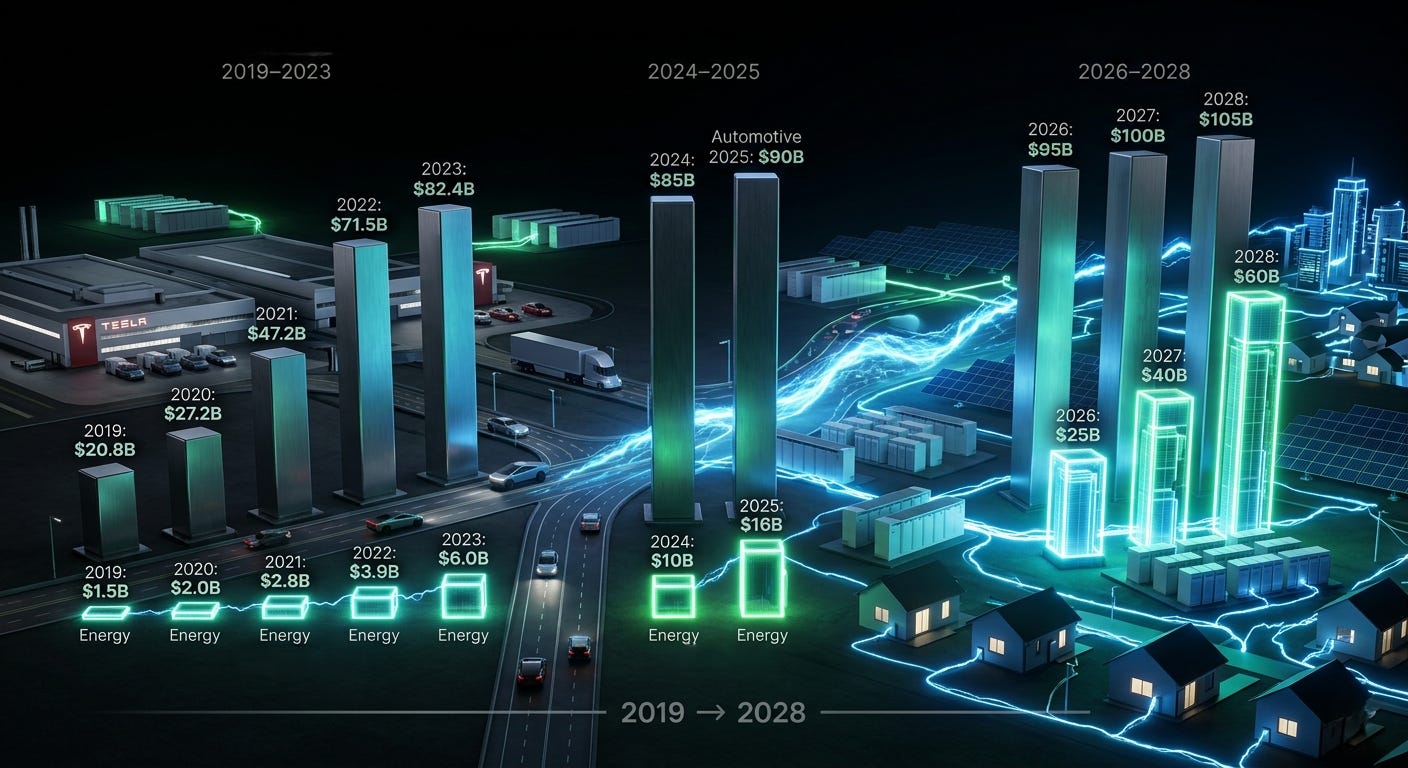

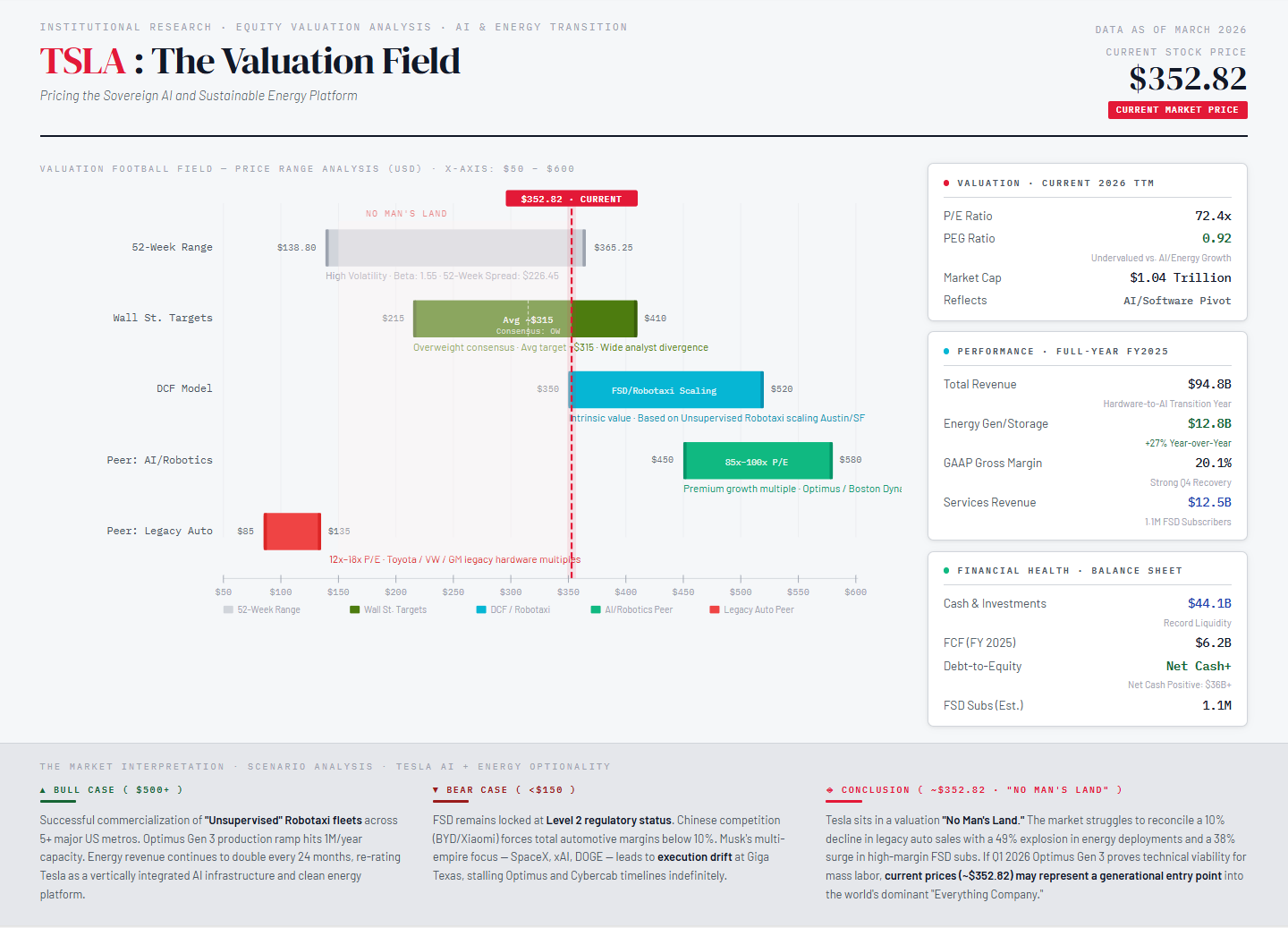

Total FY 2025 Revenue: $94.8 Billion, a slight 3% decrease year-over-year, reflecting a “transition year” as the company shifts from a hardware-centric to a physical AI business.

Automotive Sales (The Headwind): Total automotive revenues for FY 2025 were $69.5B (down 10% YoY), while Q4 results showed $17.7B, an 11% decline year-over-year. These figures were primarily impacted by a decrease in total vehicle deliveries, though the impact was partially offset by a higher vehicle average selling price and growth in other automotive ancillary sales, specifically driven by an increase in higher-margin FSD subscriptions.

Energy Generation & Storage (The Growth Engine): $12.8 Billion for FY 2025, up 27% YoY. Tesla deployed a record 46.7 GWh of storage in 2025 (up 49%), confirming Musk’s thesis that the energy business would eventually outpace automotive growth.

Revenue Eclipse (Projected Late 2030): Based on the current FY 2025 growth trajectories, where Automotive revenue declined 10 percent year-over-year to 69.5 Billion dollars and Energy revenue expanded 27 percent to 12.8 Billion dollars, the Energy division is on a mathematical path to eclipse the Automotive sector in total revenue by late 2030. This projection assumes the continued scaling of the Megapack and Powerwall businesses as the global grid transitions to sustainable storage, eventually surpassing vehicle sales as the primary top-line driver for the firm.

Profitability Eclipse (Projected Early 2028): The profitability of the Energy segment is expected to surpass that of the Automotive segment much sooner, likely by early 2028, due to significantly higher margins and lower infrastructure overhead. In Q4 2025, Energy storage gross profit reached a record 1.1 Billion dollars, benefiting from a superior margin profile compared to the Automotive sector. As the high-volume deployment of Megapacks continues to outpace vehicle margin recovery, the Energy business will become the dominant contributor to Tesla’s total GAAP Net Income well before it matches the Automotive sector in total revenue.

Services & Other (The High-Margin Tail): $12.5 Billion, up 19% YoY. This was driven by a record number of FSD subscriptions (reaching 1.1 million active subscribers, up 38%) and expanded supercharging/service revenue.

Regulatory Credits: Tesla recognized $542 Million in credits in Q4 alone, continuing to provide a pure-margin buffer for R&D.

Margin Analysis: Recovery Through Efficiency

Total GAAP Gross Margin (Q4 2025): 20.1%, a significant recovery from the 16.3% floor seen in late 2024. This 386 bp YoY increase signals that Tesla is successfully reducing per-vehicle costs even as it navigates price fluctuations.

GAAP Operating Margin: 4.6% for the full year. While down from 2024, the Q4 margin improved to 5.7% as the company absorbed higher R&D expenses related to the Optimus and Cybercab programs.

Profitability Totals: Tesla generated $4.4 Billion in GAAP operating income for the year, with a non−GAAP net income of $5.9 Billion.

Free Cash Flow (FCF) & Strategic Reinvestment

Free Cash Flow (FY 2025): $6.2 Billion, demonstrating the company’s ability to maintain liquidity while funding massive capital projects.

Cash Position: Tesla ended the year with a massive $44.1 Billion war chest (up $7.5B YoY), providing the capital necessary to weather economic cycles and invest in the “Next Wave.”

The xAI Investment: As of January 2026, Tesla entered an agreement to invest $2 Billion in xAI Series E Preferred Stock, formalizing a framework agreement to accelerate the deployment of Grok and other AI products into the physical Tesla fleet.

CAPEX: Tesla spent $8.5 Billion in capital expenditures in 2025 to build out the Cortex AI training infrastructure at Giga Texas and prepare for new production lines.

Unit Economics & The 2026 Ramp

Vehicle Deliveries: Totaled 1.636 million units for 2025. While down 9% YoY, the company successfully completed a vehicle lineup refresh, including the new Model Y.

The “Six Line” Strategy: Guidance for 2026 includes the ramp of six new production lines across vehicles, robots, energy storage, and battery manufacturing.

Optimus Industrialization: Following the January 2026 update, Tesla has officially transitioned the Optimus program from a laboratory project to a high-scale manufacturing ramp. The Gen 3 platform, unveiled earlier this year in Q1 2026, represents the first design engineered specifically for high-volume mass production. With the first dedicated production lines currently being installed, Tesla remains on track for initial production before the end of 2026, targeting an eventual long-term capacity of 1 million robots per year.

Outlook & Future Guidance

Autonomous Fleets: In January 2026, Tesla began removing safety monitors from its Robotaxis in Austin, Texas, marking the official transition to unsupervised commercial operations in select markets.

Product Timelines: Cybercab, Tesla Semi, and Megapack 3 are all confirmed to be on schedule for volume production starting in the first half of 2026.

The AI Compute Moat: Tesla plans to more than double its onsite compute capacity at Giga Texas (Cortex 2) in the first half of 2026, targeting a scale of 300,000+ H100-equivalent GPUs to maintain its lead in neural net training.

The Bull Case vs. The Bear Case

The Bull Case: The Sovereign AI Powerhouse

The Level 5 Breakthrough: If Tesla solves the “Last 1 Percent” of autonomy, the firm transitions from a hardware manufacturer to a high-margin Transportation-as-a-Service (TaaS) provider. By 2030, a global fleet of millions of Tesla vehicles could operate as an autonomous ride-hailing network, generating recurring software revenue with margins exceeding 70 percent. This effectively turns every Tesla on the road into a cash-generating asset for both the owner and the company.

Optimus and the Labor Revolution: The Gen 3 Optimus Robot represents the ultimate application of Tesla’s AI stack. If Tesla successfully scales production to 1 million robots per year as planned, they will have effectively decoupled economic productivity from human labor. By 2030, Optimus could be the primary labor force in Tesla’s own “Terafactories” and a major export for global logistics and manufacturing firms, addressing a multi-trillion-dollar labor market.

Energy as the New Grid: As the Energy Generation and Storage segment continues its 27 percent annual growth, Tesla becomes the de facto utility for the 21st century. By 2030, the Megapack and Powerwall ecosystem will likely be the foundational buffer for the world’s renewable energy grids, providing the stability required for a carbon-free global economy.

The 2030 Bull Valuation: In a scenario where Tesla dominates autonomy, labor, and energy, the company could achieve a Market Capitalization of 10 Trillion dollars or more.

Automotive: 1 Trillion dollars (as a dominant global OEM).

Energy: 2 Trillion dollars (as a global energy infrastructure provider).

Robotaxi/FSD: 4 Trillion dollars (as a high-margin software platform).

Optimus: 3 Trillion dollars (as the leader in general-purpose robotics).

Total Vision: Tesla would be the first “Everything Company,” controlling the power, the transport, and the labor of modern civilization.

The Bear Case: The Innovator’s Ceiling

The Commoditization Trap: Critics argue that as the EV market matures, Tesla will be forced into a “Race to the Bottom” on pricing. With formidable rivals like BYD and Xiaomi producing high-quality vehicles at lower costs, Tesla’s automotive margins could be permanently compressed, leaving it valued as a traditional, low-multiple car company rather than a high-multiple tech firm.

The “Last Mile” of AI: If Full Self-Driving (FSD) remains a supervised Level 2+ system indefinitely, the trillion-dollar Robotaxi thesis collapses. If technical or regulatory hurdles prevent true Level 5 autonomy, Tesla remains an OEM selling a feature rather than a platform selling a service.

Brand Polarization and “Elon Risk”: As Ashlee Vance noted in the early days, Musk is the company’s greatest asset and its greatest liability. Continued polarization of the Musk brand could alienate core buyer demographics in Western markets, allowing legacy OEMs and new entrants to capture the mission-aligned consumer base that originally built Tesla.

Capital Intensity: Unlike pure software firms, like Microsoft or Google, Tesla’s growth requires billions of dollars in physical CAPEX (8.5 Billion dollars in 2025 alone). A prolonged global recession or a spike in raw material costs could strain Tesla’s $44.1 Billion dollar cash position, slowing the R&D necessary to bring Optimus and Cybercab to market.

The 2030 Synthesis

The Deciding Factor: The delta between the Bull and Bear cases rests entirely on software execution.

If Tesla is a car company that uses AI, it is likely overvalued today.

If Tesla is an AI company that uses cars as a data-collection and distribution method, it is potentially the most undervalued enterprise in history.

By 2030, the world will know which version is the reality: a global fleet of autonomous actors and robots, or a highly efficient, yet traditional, manufacturer of sustainable hardware.

Conclusion: The “End State”

The End of Scarcity: Beyond the spreadsheets and the production targets lies a vision of a world where the fundamental constraints of human history, energy and labor, are finally solved. Through the convergence of the Megapack’s infinite storage and the Optimus robot’s tireless labor, Tesla is architecting a future of sustainable abundance. In this version of 2030, the cost of living drops toward the cost of electricity, and the most grueling, dangerous tasks of our civilization are handed off to machines that never tire and never complain.

The Earthly Proving Ground: As we have seen through the lens of Ashlee Vance’s biography, Musk’s ambitions have always been larger than a single planet. Tesla is not merely a commercial enterprise; it is the earthly proving ground for the technologies required to sustain life in the most hostile environments imaginable. The batteries that power a home in Austin and the robots that walk the floors of Giga Texas are the direct ancestors of the life-support systems and automated workforce that will eventually build the first cities on Mars.

The Logic of Optimism: It is easy to be a cynic in a world of stranded assets and innovator’s dilemmas, but Tesla’s journey proves that First Principles thinking combined with an extraordinary threshold for pain can bend the arc of history. We are witnessing the moment where science fiction ceases to be a dream and begins to roll off an assembly line. This is the “hardcore” reality of progress: a relentless, engineering-led drive toward a future where humanity is no longer a passenger to environmental decay, but the master of its own sustainable destiny.

The Survival of Human Consciousness: Ultimately, to invest in or even to observe Tesla is to participate in a grand experiment regarding the meaning of life and the survival of consciousness. By accelerating the transition to sustainable energy and pioneering the age of Physical AI, Tesla is ensuring that our civilization remains vibrant and capable enough to reach for the stars. The transformative milestones of 2026 are just the beginning of a story that ends with humanity becoming a multi-planetary species, finally securing its place among the light of the universe.

Gannon Capital Final Thoughts: Following Elon Musk for over a decade has taught me that he is the rare founder who treats failure as a refinery. He has survived trials that would have collapsed any other CEO, emerging every time with a larger moat. Nvidia’s Jensen Huang recently summed up the industry’s respect for him perfectly: “I’ll take a phone call from him any time... I’d be happy to be involved in anything he does.”

While I do not expect a phone call from Elon anytime soon, I will always be more than comfortable betting on any enterprise he leads.

Receipts: Putting My Money Where My Mouth Is

As always, I have included receipts for all my purchases while hiding the quantity of shares and my account number for privacy.

My current position is at an average price per share of $169.48.

Note: I have to give credit to my wife, Erin (ValleyMeadow), for suggesting that we invest in Tesla in the first place. She began investing in the company long before I did and her position is more substantial than my own. Thank you my love!

Disclaimer:

I’m not your financial advisor, your lawyer, or your life coach (though I do wish you well). This content is for informational and entertainment purposes only. It is not financial advice, and it should not be treated as such. Investing involves risk, including the risk of losing your money, your patience, and possibly your hair. Always do your own research, consult with licensed professionals, and never invest more than you can afford to lose.