Cava Group Deep Dive

Chipotle 2.0 - A Look into the Mediterranean Fast-Casual Empire

Cava Group - The Chipotle 2.0 Story

On February 24, 2026, CAVA Group achieved a major milestone few fast-casual restaurants ever reach: crossing the $1 billion annual revenue mark.

Despite a challenging “K-shaped” economy, CAVA reported 22.5% full-year top-line growth and jaw-dropping restaurant-level margins of 24.4%.

The market rewarded this execution immediately, sending CAVA shares soaring 24% the very next day.

Why this Matters

Finding the “next Chipotle” has been Wall Street’s favorite obsession for a decade, with dozens trying and failing to replicate the high-throughput, healthy food model.

CAVA is proving that it is actively defining the Mediterranean fast-casual category for the public markets.

The company is currently executing a masterclass in unit economics, brand loyalty, and scaling, making it one of the most important consumer growth stories to study right now.

Origin Story: Maxed-Out Credit Cards & Crazy Feta

Picture the mid-2000s. If you wanted Mediterranean food, you had two choices: a sketchy 2 AM falafel cart, or a stuffy, white-tablecloth Greek restaurant. There was no cool, approachable middle ground.

Enter Ike Grigoropoulos, Chef Dimitri Moshovitis, and Ted Xenohristos. These three childhood friends, all children of Greek immigrants, decided to fix that. In 2006, they maxed out their credit cards and opened Cava Mezze, a single, 60-seat sit-down restaurant in Rockville, Maryland.

After a slow first few weeks and building a client base through word-of-mouth advertising about the delicious food and charming hospitality, the restaurant became a smash hit. Lines spilled out the door, and customers were literally begging to buy tubs of their fiery, addictive “Crazy Feta” dip to take home.

The three friends quickly hit a wall as sit-down restaurants are a total nightmare to scale. You can’t just clone the founders and expect the magic to duplicate across the country.

The Pivot

Realizing they were bottlenecked, they brought on Brett Schulman as CEO in 2010. Schulman, who had a background in finance and snack foods, did a lot more than just tweak the menu; he completely blew up the business model.

He executed a genius, dual-pronged pivot:

The Fast-Casual Playbook: He helped distill their complex, sit-down menu into a highly scalable, Chipotle-style assembly line. The first fast-casual “CAVA” opened in 2011.

The Grocery Hustle: He packaged up their legendary Crazy Feta and Hummus and got them onto the shelves at Whole Foods.

CAVA had transformed from a popular local dinner spot into a dual-threat empire: a high-margin restaurant chain with a grocery business acting as a paid national billboard.

Gannon Capital Internal Thoughts: The story behind CAVA is one of love, determination and resilience. As children of kitchen workers, the trio spent their early years in various food service jobs that shaped their view on how restaurants should be run and how employees should be treated.

Funding Cava Mezze meant taking massive financial risk and quite literally going all in on their idea. On top of maxing out their credit cards, one of the friends even sold their Jeep that they had recently won in a Church raffle; perhaps God’s way of helping out financially.

When it came time to build the restaurant, hiring a construction crew was out of the question due to capital constraints, so the three friends literally built it with their bare hands.

The restaurant was tucked-away in a half-empty shopping center inside an old Russian bakery, a space that location experts would have dubbed “doomed to fail” before they even opened their doors.

In 2008 they secured a bank loan to help sustain operational costs, but it was later withdrawn due to the financial crisis, leaving them to scratch and claw for alternative financing and private loans to keep the business afloat.

These early hardships are often cited by the founders as the reason for Cava’s “hospitality-first” culture. They lived the reality of the underdog for years before the fast-casual pivot in 2011 made them a household name.

History

The Grocery Aisle Hack

How do you get people to eat at a restaurant they’ve never heard of? You sneak your way into their fridge first.

While CAVA was methodically opening new fast-casual locations, they were also heavily pushing their signature dips into Whole Foods and local grocers. It was a genius, self-funding marketing engine. By the time a physical CAVA location finally opened in a new suburb, locals already knew the brand because they had been eating Crazy Feta in their living rooms for months.

The Zoës Kitchen “Heist” (2018)

Here is the hard truth about the restaurant business: building physical locations from scratch is painfully, agonizingly slow. Between zoning, permits, and construction, it takes forever.

To side-step this process, in 2018 CAVA pulled off one of the smartest real estate plays in modern restaurant history. They acquired a struggling, much larger rival named Zoës Kitchen for $300 million.

CAVA didn’t want Zoës’ menu or its brand. They wanted its incredibly prime, suburban real estate. Instead of fighting for new leases, CAVA spent the next five years methodically gutting Zoës locations and flipping them into high-performing CAVAs. It was the ultimate Trojan Horse.

They effectively bought a five-year “fast-forward” button for their national expansion.

The Blockbuster IPO (2023)

By June 2023, the Zoës conversions were humming, the unit economics were printing cash, and Wall Street was absolutely starving for a hot consumer brand.

CAVA went public in a blockbuster IPO, pricing above its target range and nearly doubling on its first day of trading. They proved they could scale a niche Greek cuisine into a national powerhouse.

The Business: What They Do

The “Walk-The-Line” Masterpiece: CAVA operates a rapidly expanding empire of fast-casual Mediterranean restaurants. They use the highly customizable, assembly-line model (think “Chipotle, but Mediterranean”). You walk the line, point at what you want, and get your food in minutes.

The Menu Magic: It all starts with a base of hearty grains, greens, or a warm pita. Then comes the good stuff: premium proteins (like Harissa Honey Chicken or grilled steak) that get absolutely smothered in their proprietary, flavor-bomb dips and dressings, like Tzatziki, Skhug, and the legendary Crazy Feta.

The Profitable Side Hustle: CAVA doesn’t just wait for you to come to them; they have already claimed a spot in your grocery aisle. Their lucrative Consumer Packaged Goods (CPG) business sells those signature dips in supermarkets nationwide. This creates a profitable, edible billboard that builds brand addiction at home.

A Digital Juggernaut: No one likes waiting behind a guy ordering lunch for his entire office. CAVA solves this by driving nearly 38% of its sales through digital channels. They keep operations lightning-fast by using dedicated “digital make-lines” hidden in the kitchen and rolling out highly efficient drive-thru pickup windows, “CAVA Pick-Up Lanes”, to get hungry digital customers in and out seamlessly.

The Thesis: Why Wall Street is Obsessed

The Massive White Space: If you want a burger, chicken sandwich, or a burrito, you have fifty choices on every highway in America, but fast-casual Mediterranean simply didn’t exist. CAVA owns this space outright and are the undisputed heavyweight champion of a cuisine with massive, untapped geographical white space.

Generational Tailwinds (The “Anti-Junk” Movement): Younger demographics are actively ditching sad, greasy drive-thru meals. Consumers are demanding “food as medicine”, ingredients that are vibrant, fresh, ethically sourced, and actually make them feel good after eating (without sacrificing bold flavor). CAVA surfs this macroeconomic health wave perfectly.

The 1,000-Store Roadmap: Wall Street loves a predictable, massive growth story. Closing out 2025 with 439 locations, management isn’t just throwing darts at a map. They have a surgical, highly proven blueprint to hit 1,000 restaurants by 2032. They know exactly how to parachute into a new market, build hype, and win.

Cash-Printing Unit Economics: This is the absolute holy grail of the restaurant industry. CAVA’s store-level margins are so wildly efficient that almost every time they cut the ribbon on a new location, it is highly accretive to the bottom line. They aren’t burning millions just to grow and have a self-funding culinary empire.

The Competition

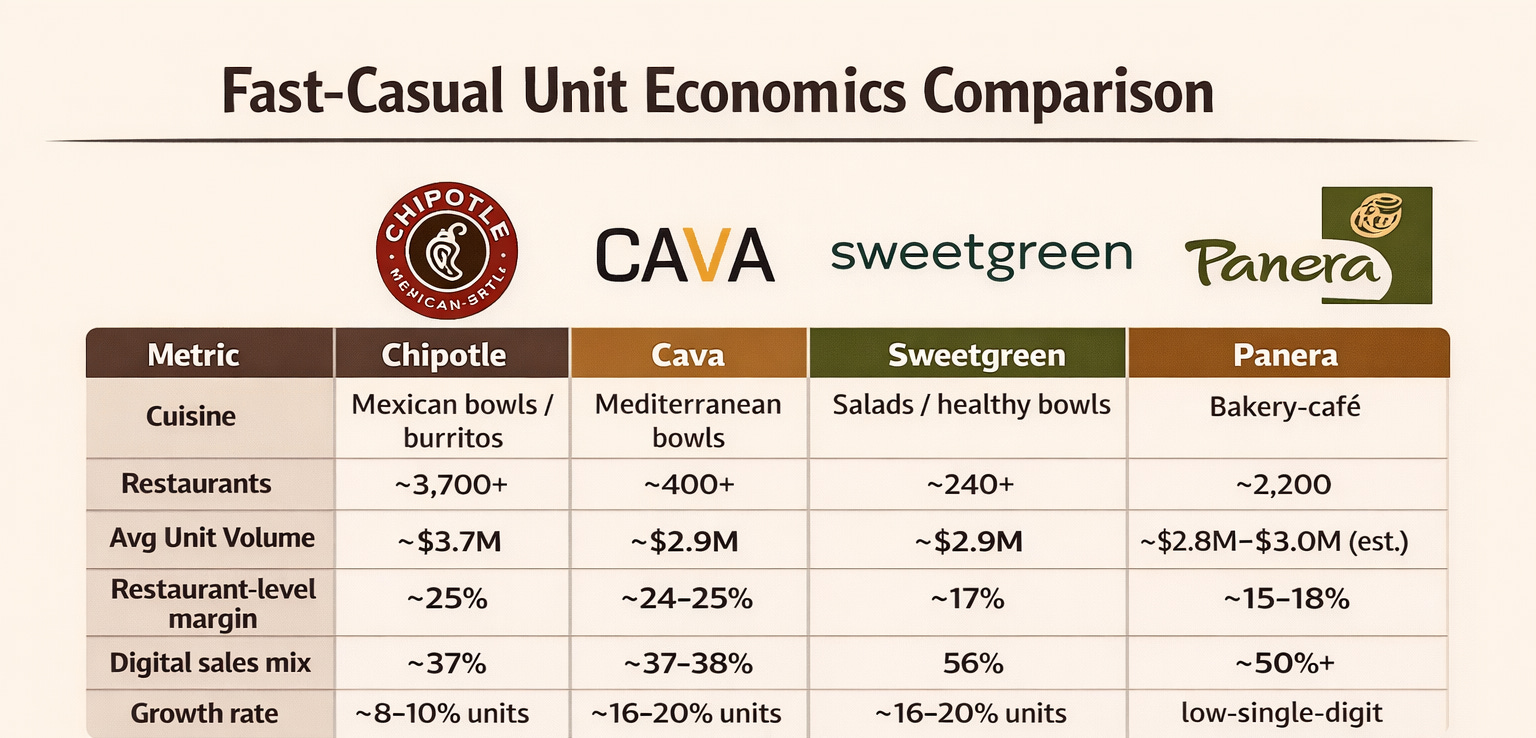

Chipotle (The Gold Standard): Chipotle is the reigning king of the fast-casual mountain, and make no mistake, CAVA is hunting for the exact same Millennial and Gen-Z dollar. CAVA differentiates itself by offering a vastly different flavor profile and a much stronger wellness aesthetic.

The CAVA Edge: The “Food Coma” Immunity. While a massive steak burrito might require a 3 PM nap, CAVA rides an untouchable, organic health halo. The Mediterranean Diet has been ranked the #1 overall diet by U.S. News & World Report for seven consecutive years. CAVA doesn’t even have to spend marketing dollars to convince you their food is healthy; doctors and scientists have already done it for them.

Chipotle has also been linked to several high-profile foodborne illness outbreaks including norovirus, Salmonella, and E. coli. This phenomenon became so well-known that South Park even did a skit on it back in 2009; the infamous “Chipotlaway” episode.

Sweetgreen (The Trendy Rival): Sweetgreen is the direct competitor in the premium “health and wellness bowl” space. But while Sweetgreen has the aesthetic down, they have historically struggled with the actual business of restaurants, namely, profitability and consistent foot traffic.

The CAVA Edge: The Dinner Time Dominance. Sweetgreen is notoriously a lunch-hour phenomenon; their stores often turn into ghost towns after 2 PM because most people don’t crave cold kale for dinner. CAVA, on the other hand, boasts a nearly perfect 50/50 split between lunch and dinner sales because they offer warm, hearty, “crave-able” proteins. This balanced traffic flow is exactly why CAVA’s 24%+ margins utterly dwarf Sweetgreen’s historically lower profitability.

Panera / Chopt / Legacy Chains (The Old Guard): These are the legacy lunch-hour staples fighting for the suburban and city office worker market. These chains are aging rapidly, lack cultural momentum, and are struggling with massive operational bloat.

The CAVA Edge: Centralized Kitchen Sorcery. Legacy giants like Panera have recently been forced to slash dozens of items from their menus because their kitchens simply couldn’t handle the operational complexity. CAVA manages to serve incredibly complex, labor-intensive foods (like fire-roasted eggplant and whipped feta) seamlessly at scale. How? Because CAVA owns its own centralized manufacturing facilities. They make the complicated dips off-site and ship them to the stores, removing the operational complexity from their local restaurants while the old guard trips over its own feet.

Gannon Capital Internal Thoughts: As far as margins are concerned, Cava is on par with Chipotle. The main KPI that interests me is their growth rate, which is currently double Chipotle’s. That’s not the only reason I am choosing Cava over their Mexican competitor. Chipotle’s stock has been in a volatile decline for the past two years. Since peaking in June 2024, the stock has dropped approximately 50% and Cava is capitalizing on their shortfalls.

Reasons for Chipotle’s decline:

Falling Foot Traffic: Four straight quarters of declining customer visits throughout 2025.

Squeezed Demographics: Core Gen Z, Millennial, and middle-income diners pulled back due to inflation and tighter budgets.

Slashed Guidance: Management lowered expectations, projecting essentially flat same-store sales for 2026.

Shrinking Margins: Rising wages and surging commodity costs (like beef and avocados) ate into profitability.

Loss of Pricing Power: Forced to halt aggressive menu price hikes to avoid driving away price-sensitive customers.

Valuation Reset: Stalling growth violently popped the stock’s “priced-for-perfection” 50x P/E multiple.

Leadership Shakeup: The 2024 departure of rockstar CEO Brian Niccol, who was poached to lead Starbucks, left leadership vulnerable during a tough economic cycle.

Quality Matters: What does the consumer think?

Based on recent aggregated reviews across all U.S. locations, here is where each of these fast-casual restaurants’ average Google Review star ratings currently sit:

CAVA: 4.5 Stars: Consistently the highest rated of the group. Reviews heavily praise the food quality, customizable options, and friendly staff, though negative reviews usually point to the premium price tag or occasional inconsistent portion sizes.

Sweetgreen: 4.2 Stars: Strong ratings overall, largely driven by the health halo and ingredient freshness. However, scores are frequently dragged down by complaints regarding high prices, small portions, and lunch-hour wait times.

Chipotle: 3.7 Stars: Based on an aggregation of over 2.3 million reviews across 2,500+ locations. While the food remains incredibly popular, a surge in complaints over the last two years regarding shrinking portion sizes, messy dining rooms, and missing digital-order ingredients has dragged their brand-wide average down.

Panera Bread: 3.8 Stars: The lowest of the group. Legacy locations suffer from operational bloat. Frequent complaints point to deteriorating food quality compared to 10 years ago, high prices for basic items (like half-sandwiches), and slow service during peak hours.

The Moat

The Secret Sauce Factory (Vertically Integrated Supply Chain): Making authentic Mediterranean food is brutally labor-intensive. Roasting eggplant, whipping feta, and perfectly balancing the garlic in tzatziki takes hours of prep. If CAVA relied on teenagers in 400+ local kitchens to make these complex recipes from scratch every morning, labor costs would explode and quality would be a coin toss at best.

The Convincing Story: CAVA completely bypassed this operational nightmare by building its own centralized manufacturing facilities. They make the complex dips off-site and ship them to the stores. This both slashes back-of-house labor costs and protects their proprietary flavor IP. This ensures that the Crazy Feta in Dallas tastes exactly as mind-blowing as it does in Boston. It is a massive, capital-intensive logistical moat that a new competitor cannot replicate overnight.

The Economic Shock Absorber (Best-in-Class Unit Economics): In the restaurant industry, margins are the ultimate defense mechanism. CAVA is currently cranking out eye-watering Average Unit Volumes (AUVs) of $2.9 million with restaurant-level profit margins of over 24%.

The Convincing Story: Why is this a moat? Because it acts as an impenetrable shock absorber. When macroeconomic chaos hits, whether it’s soaring beef prices, minimum wage hikes, or agricultural tariffs, a competitor operating on razor-thin 10% margins is instantly pushed to the brink of bankruptcy. CAVA, with its fat 24% cushion, just absorbs the blow, smiles, and keeps aggressively funding its 1,000-store expansion while its rivals play defense.

Escaping the Discount Doom Loop (The “Everyday Value” Brand): Look at the rest of the fast-food industry right now. Everyone is panicking, slashing prices, and rolling out desperate $5 “Value Meals” to win back lower-income consumers. This creates a toxic cycle: you destroy your margins and train your customers to only show up when they have a coupon.

The Convincing Story: CAVA doesn’t play that game. They have cultivated such fierce, organic brand loyalty and high perceived food quality that they maintain absolute pricing power. Customers walk in because they want a premium, customized, healthy meal, and they are perfectly happy to pay full price for it. In a hyper-competitive economy, the ultimate moat is a customer base that happily ignores your competitor’s coupons.

Old-School Hospitality (The “Love Button”): While legacy fast-food chains are aggressively replacing cashiers with AI kiosks and facing viral TikTok backlashes over shrinking portions, CAVA is playing a completely different game. Since their first store, every CAVA cash register has featured a “Love Button”. Management empowers front-line workers to hit this button and comp a meal for free if a customer is having a bad day, forgot their wallet, or is just a loyal regular. It costs the company pennies on the dollar in food costs, but the ROI is staggering. It generates fierce, organic brand loyalty and viral social media marketing that competitors spending billions on ad campaigns simply cannot replicate.

Strategic Partnerships & Alliances

Whole Foods & National Grocers: A symbiotic relationship where grocery placement acts as paid advertising, introducing suburban shoppers to the brand before a physical restaurant opens.

How it started: This massive retail presence began in 2010 when CEO Brett Schulman leveraged his prior snack-food industry connections to pitch regional Whole Foods buyers, literally hand-delivering tubs of their signature “Crazy Feta” to prove local demand.

The Financial Impact & Growth: The Consumer-Packaged Goods (CPG) division generates roughly $35 to $40 million in direct annual revenue. More importantly, it is projected to grow at a steady 15-20% YoY as they expand into new grocery chains, acting as a self-funding customer acquisition tool that funnels hungry shoppers directly to their physical restaurants.

Tech Integrations (Digital & Loyalty): Utilizing a revamped, data-driven loyalty program with tiered status levels (including an invite-only “Oasis” tier) to capitalize on their high digital revenue mix.

How it started: CAVA’s internal digital team partnered with top-tier restaurant tech platforms to completely overhaul their aging app, transitioning from a basic “spend-to-earn” model into a highly personalized digital engine that tracks specific dietary habits.

The Financial Impact & Growth: This digital ecosystem is an absolute cash cow, driving nearly 38% of CAVA’s total sales, equating to an immense $444 million of their FY2025 revenue. While third-party delivery fees can drag on profitability, CAVA protects its bottom line with a 15% delivery menu markup. More importantly, their massive volume of direct-app pickup orders act as the company’s highest-margin transactions (often yielding margins in the high 20s to low 30s) due to lower labor needs and a 10-15% higher average check size.

Killer KPI: With the rollout of dedicated “CAVA Pick-Up Lanes,” management expects this highly profitable digital mix to push past 40%. This absolutely crushes their competition’s margins.

Supply Chain Partners: Deep partnerships with local suppliers and international vendors to maintain their farm-to-table aesthetic while navigating complex ingredient sourcing and tariffs.

How it started: The founding trio bypassed massive corporate food distributors early on to shake hands directly with boutique Greek olive oil producers and local farmers, securing exclusive pipelines for authentic ingredients competitors can’t access.

The Financial Impact & Growth: While not a direct revenue line, this direct-sourcing and centralized prep model is the sole reason CAVA can protect its jaw-dropping 24% restaurant-level profit margins and support $2.9 million Average Unit Volumes (AUVs). Their current centralized manufacturing footprint is actively scaling, with enough capacity already built out to efficiently support up to 750 locations as they march toward their 1,000-store roadmap.

The Numbers

(Reported Feb 24, 2026, for Fiscal Year 2025)

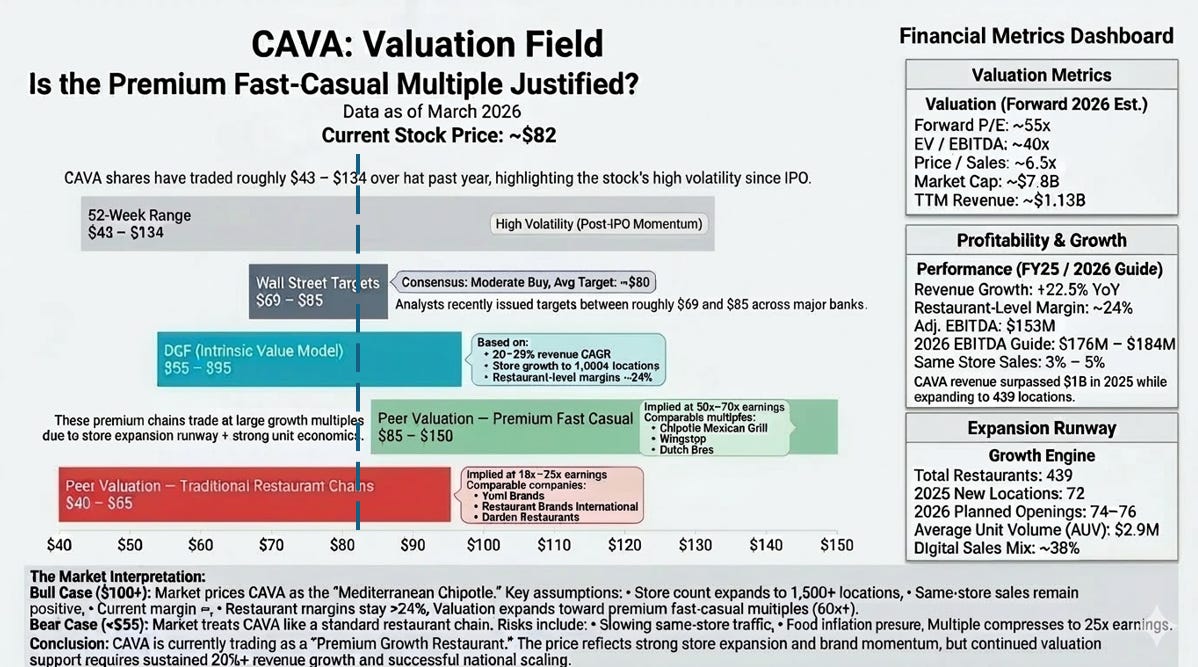

Total Revenue: $1.169 billion (+22.5% YoY growth)

Total Locations: 439 (Added 72 net new restaurants in 2025)

Average Unit Volume (AUV): $2.9 million per store

Restaurant-Level Profit Margin: 24.4%

Adjusted EBITDA: $152.8 million

Same-Restaurant Sales: +4.0% for the full year (with Q4 up 0.5%, defying Wall Street’s expectations of a decline)

The 2026 Outlook (Guidance & Forward Profitability): Management projects continued high-octane growth for Fiscal 2026, guiding for 74 to 76 net new restaurant openings and a solid same-restaurant sales growth of 3% to 5%. Even while absorbing the costs of new market expansion and the launch of premium seafood, they expect to fiercely protect their industry-leading profitability, forecasting restaurant-level margins between 23.7% and 24.2%

Valuation & Risks

Priced for Perfection (The Multiple Trap): Wall Street is absolutely in love with CAVA, but that love comes at a cost. Following its massive earnings surge, the stock is trading at a premium, boasting an enterprise value north of $8.3 billion and a forward P/E multiple that rivals high-flying tech stocks. When you are priced this aggressively, you are priced for flawless, uninterrupted dominance. There is zero margin for error. Any slight operational misstep, or even a minor delay in new store openings, could trigger a brutal and violent multiple compression.

Traffic Concerns (The Footfall Squeeze): Top-line beats are great, but peeking under the hood reveals a slight vulnerability. While Q4 2025 same-store sales technically eked out a +0.5% gain, that growth was propped up by higher menu prices and product mix. Actual foot traffic in the broader fast-casual industry is facing intense pressure as the “K-shaped” economy squeezes the middle class. If consumer spending retracts further and diners start trading down or eating at home, CAVA won’t be able to rely solely on higher ticket prices to keep their growth engine running.

Margin Pressures (Defending the 24%): Achieving industry-leading 24.4% restaurant-level margins is incredible; defending them year after year is the hard part. CAVA is actively rolling out higher-cost, premium proteins, like Q1 2026’s highly anticipated new Pomegranate-glazed Salmon, which naturally carry tighter profit margins. Combine that with the looming threat of complex agricultural tariffs on imported Mediterranean ingredients (like olive oil and spices) and the continuous creep of wage inflation, and management will have to execute a supply chain masterclass to keep those profits from eroding.

Scaling Execution (The Middle-America Test): The “1,000-Store Roadmap” looks fantastic on a boardroom slide, but reality is geographically messy. Growing from 439 locations to over 1,000 means CAVA can no longer just rely on affluent coastal cities and high-income metropolitan suburbs. They have to push deep into middle-American “B” and “C” tier markets. The ultimate execution risk lies here: Will the everyday consumer in the Midwest or the Sunbelt embrace a $14 Harissa Honey Chicken and Crazy Feta bowl with the same rabid enthusiasm as a tech worker in Austin or San Francisco?

Final Thoughts

When CAVA went public in 2023, critics dismissed it as just another overhyped “hummus and pita” chain. By early 2026, those same critics watched in awe as the company crossed $1 billion in annual revenue, posted jaw-dropping 24.4% margins, and saw its stock surge 24% in a single day.

This matters because CAVA has completely defied the current restaurant industry playbook. While legacy fast-food giants are panicking and rolling out desperate $5 value meals to win back inflation-weary customers, CAVA is proving that consumers will still happily pay full price because their products are actually worth it.

CAVA didn’t build a cash-flowing juggernaut by accident. They executed a masterclass in operational leverage: using a “Trojan Horse” real estate strategy to scale fast, vertically integrating their supply chain to protect their complex flavors, and building a lucrative grocery business that doubles as a national billboard. They achieved the impossible in the restaurant world by taking a niche ethnic cuisine and standardizing it for the masses without stripping away its soul.

Look at your own business, career, or investment portfolio through the CAVA lens: Are you competing on price, or are you competing on value? If you find yourself constantly discounting just to get people through the door, you are playing a losing game. Stop racing to the bottom and start building an unbreachable moat around uncompromising quality.

CAVA is currently trading at a 150x forward P/E multiple because Wall Street believes they are the definitive “Next Chipotle.” Are you willing to pay a massive premium for a best-in-class, flawlessly executing brand, or is this valuation simply too rich for your blood?

Let me know in the comments.

Receipts: Putting My Money Where My Mouth Is

As always, I have included receipts for all my purchases while hiding the quantity of shares and my account number for privacy.

My current position is at an average price per share of $46.85.

Disclaimer:

I’m not your financial advisor, your lawyer, or your life coach, though I do wish you well. This content is for informational and entertainment purposes only. It is not financial advice, and it should not be treated as such. Investing involves risk, including the risk of losing your money, your patience, and possibly your hair. Always do your own research, consult with licensed professionals, and never invest more than you can afford to lose.