AMD Deep Dive

The civil war for the future of AI

The AMD Origin Story: “Real Men Have Fabs”

To understand AMD’s current war against Nvidia, you must understand its birth as the eternal underdog. The company was defined by a quote from its founder, Jerry Sanders, who famously mocked fabless chip designers: “Real men have fabs.”

The irony is that AMD only found salvation 40 years later by selling those fabs, while its arch-rival Intel began to crumble under the weight of keeping them.

The Fairchild Exodus

In 1968, the “Golden Boys” of Fairchild Semiconductor, Robert Noyce and Gordon Moore, left to found Intel. They were scientists, backed by immense capital, with a mission to invent the future.

A year later, Jerry Sanders led his own exodus from Fairchild to found AMD. Sanders wasn’t a scientist; he was a flamboyant sales director. He didn’t have a breakthrough product or the VC elite behind him. What he had was a Rolodex and a refusal to die. From day one, the dynamic was set: Intel was the Aristocrat, defined by innovation. AMD was the Scrapper, defined by hustle.

The “Second Source”

AMD’s early strategy wasn’t invention; it was survival. In the early computing era, military and enterprise customers (like IBM) refused to rely on a single supplier. They demanded a “second source”, a backup manufacturer to keep supply chains secure.

AMD filled this void, becoming the licensed manufacturer of chips designed by others. For decades, this relegated AMD to the role of “Intel’s Waiter.” They subsisted on the crumbs of the x86 market, reverse-engineering Intel’s designs and selling compatible chips at a discount. They were the budget option, the generic brand.

The Sanders Culture

Sanders knew he couldn’t out-spend Intel on R&D, so he built a culture to out-last them. Famous for his white suits, Rolls Royces, and lavish parties, Sanders operated on a simple philosophy: “People first, products and profit will follow.”

It was a survival mechanism. To stop engineers from defecting to the wealthier Intel, Sanders gave equity to everyone, from top designers to line workers. This created a fiercely loyal, tribal culture. Even today, under CEO Dr. Lisa Su, AMD operates with the muscle memory of a company that remembers trading at $2.00, fighting for its life against a monopoly.

The History: From Near-Death to Resurrection

If the Sanders era was defined by salesmanship, the decade that followed was defined by survival.

The Lost Decade (2006–2014)

The ATI Acquisition (2006): AMD bought graphics company ATI for $5.4 billion. At the time, Wall Street viewed the deal as a disaster; AMD overpaid significantly and took on crushing debt just before the 2008 financial crisis.

The Irony: That “disastrous” deal is the only reason AMD is a player in the AI race today. It provided the GPU intellectual property needed to challenge Nvidia, something Intel is still struggling to replicate.

The Spin-Off (2009): To survive the debt load, AMD had to abandon its founder’s creed “Real men have fabs”. The company spun off its manufacturing arm into GlobalFoundries, officially going “fabless.” While humiliating at the time, this structural shift allowed AMD to stop bleeding cash on factories and eventually partner with TSMC.

The Low Point (2015): Following the flop of its “Bulldozer” CPU architecture, the stock traded as low as $1.61. The company was burning cash, buried in debt, and dismissed by the market as “uninvestable.”

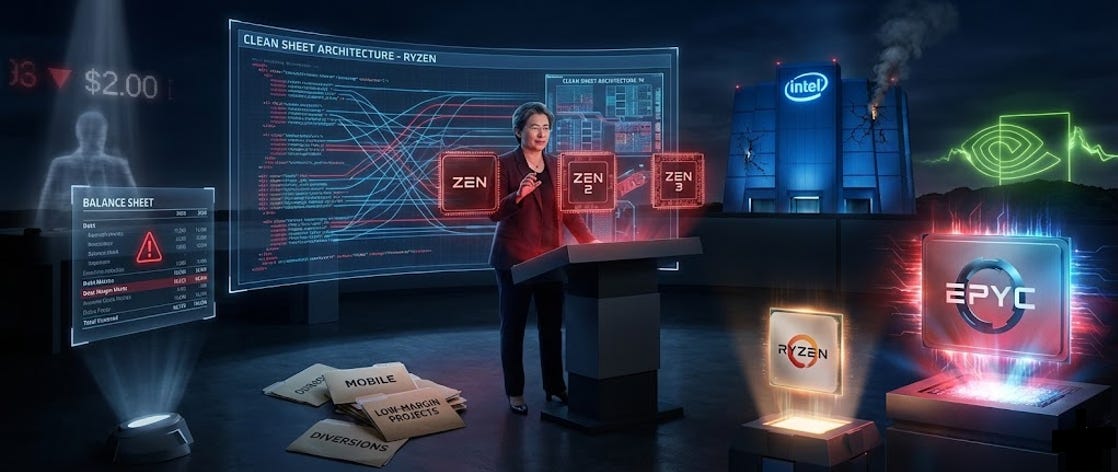

The Lisa Su Turnaround (2014–Present)

The Pivot: In 2014, Dr. Lisa Su (an MIT-trained electrical engineer) took the helm. Unlike previous sales-focused CEOs, she engineered her way out of the crisis. She mercilessly cut distracting projects, like mobile chips, to bet the entire company on one thing: High-Performance Computing (HPC).

The Zen Moment: The turnaround hinged on a “clean sheet” CPU design called “Zen.” It was a moonshot, and if it failed, bankruptcy was likely.

The Result: Launched in 2017 under the brand Ryzen, and later EPYC for servers, Zen shocked the industry. For the first time in a decade, AMD matched Intel’s performance at a fraction of the power and cost, initiating a structural erosion of Intel’s monopoly that continues today.

The Business: What AMD Actually Does

AMD reports revenue in four distinct segments. While they started as a PC company, the investment story has shifted entirely to the Data Center.

Data Center (The Crown Jewel)

This is the engine driving the stock price and margin expansion.

EPYC CPUs (Server): AMD has successfully “flipped the script” on Intel in the cloud.

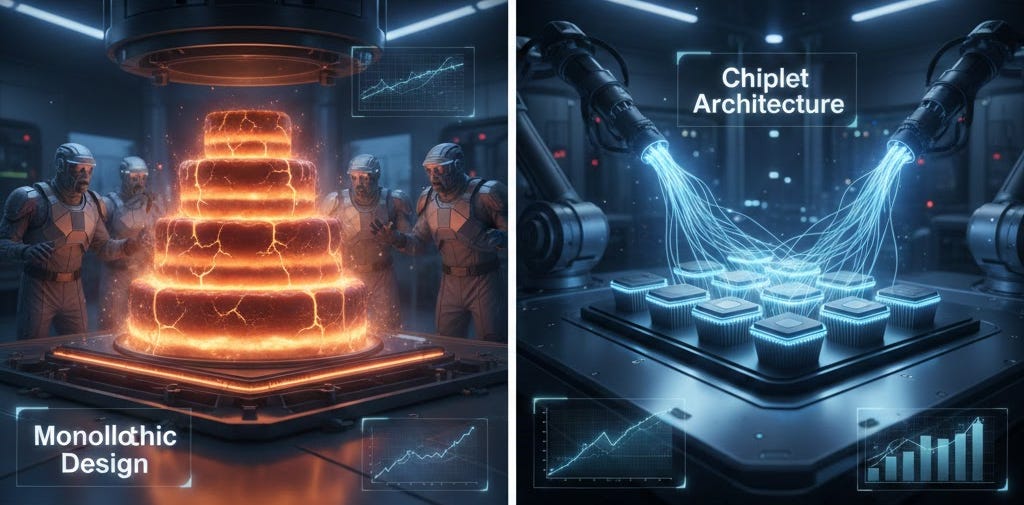

The Edge: By using a “chiplet” design (gluing smaller chips together), EPYC offers more cores and better power efficiency than Intel’s monolithic Xeon processors.

The Result: AMD has gone from less than 1% server market share in 2017 to over 33% today. They power the mission-critical workloads for AWS, Azure, Google Cloud, and Meta.

Instinct GPUs (The AI Play): The MI300 series is the specific product challenging Nvidia’s H100 monopoly.

The Ramp: It is the fastest-ramping product in AMD history, hitting $1 billion in sales in record time. It is the industry’s only viable “second source” for training Large Language Models (LLMs).

Client (PCs)

Ryzen Processors: These chips power consumer laptops and desktops.

The Cycle: After a massive COVID boom and a subsequent hangover, this segment is stabilizing.

The Catalyst: The emergence of the “AI PC”, laptops with built-in Neural Processing Units (NPUs) to run AI locally, is driving a new upgrade cycle for commercial and consumer devices.

Gaming

Radeon GPUs: AMD is the only company that competes with Nvidia in discrete graphics cards for gamers, though they hold a minority share (typically 10-20%).

Semi-Custom (Consoles): AMD holds a unique monopoly here. They design the custom silicon for both the Sony PlayStation 5 and the Microsoft Xbox Series X/S.

The Dynamic: This revenue is highly cyclical (peaking at console launch, fading late-cycle), but it provides reliable, high-volume cash flow to fund R&D elsewhere.

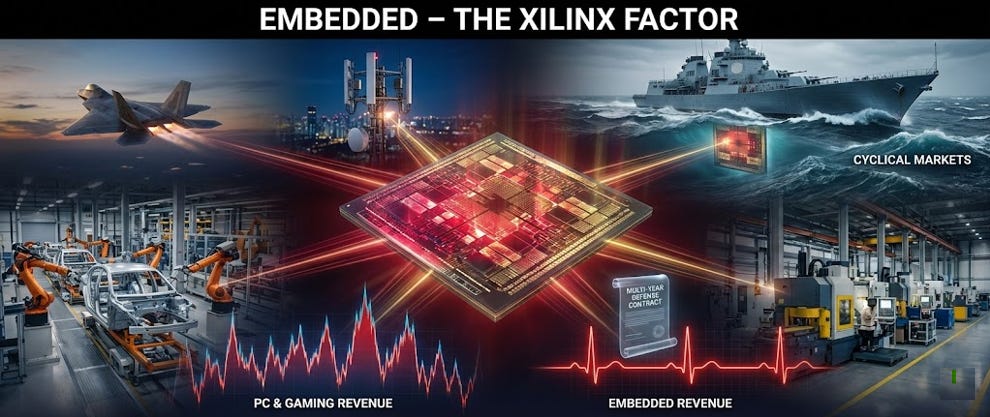

Embedded (The Xilinx Factor)

The Acquisition: In 2022, AMD acquired Xilinx for $49 billion, the largest deal in semi history at the time.

What it Does: Xilinx makes FPGAs (programmable chips) for markets that don’t change every year: Aerospace, Defense, Automotive, and Industrial.

Why it Matters: This segment is the stabilizer. While PC and Gaming revenue can be volatile, Embedded contracts last for years (e.g., a chip in an F-35 fighter jet or a 5G tower), smoothing out AMD’s overall financial profile.

The Thesis: The “Everything Else” Trade

The investment case for AMD expands beyond its own technology; it’s about the market structure.

The world needs an alternative to the giants.

The Anti-Nvidia

The Hyperscaler Dilemma: Microsoft, Meta, Google, and Amazon are spending tens of billions on AI hardware. Currently, they are beholden to Nvidia, which dictates pricing and allocation. They are desperate for leverage.

The Second Source: History is repeating itself. Just as IBM needed AMD to check Intel in the 80s, the Hyperscalers need AMD to check Nvidia today. Even if the MI300 is only 80% as good as Nvidia’s H100, the biggest companies in the world will buy it to diversify their supply chain and keep Jensen Huang’s pricing honest.

The Intel Donor Cycle

Structural Share Gains: For decades, AMD’s market share gains were cyclical; one good chip, then a fade. This time is different. AMD’s move to chiplets and TSMC manufacturing has created a structural lead over Intel.

The Math: The server CPU market is massive. Every 1% of market share AMD takes from Intel is worth billions in high-margin revenue. Intel is currently fighting a war on two fronts (manufacturing and design), leaving their datacenter dominance vulnerable to continued erosion.

Margin Expansion

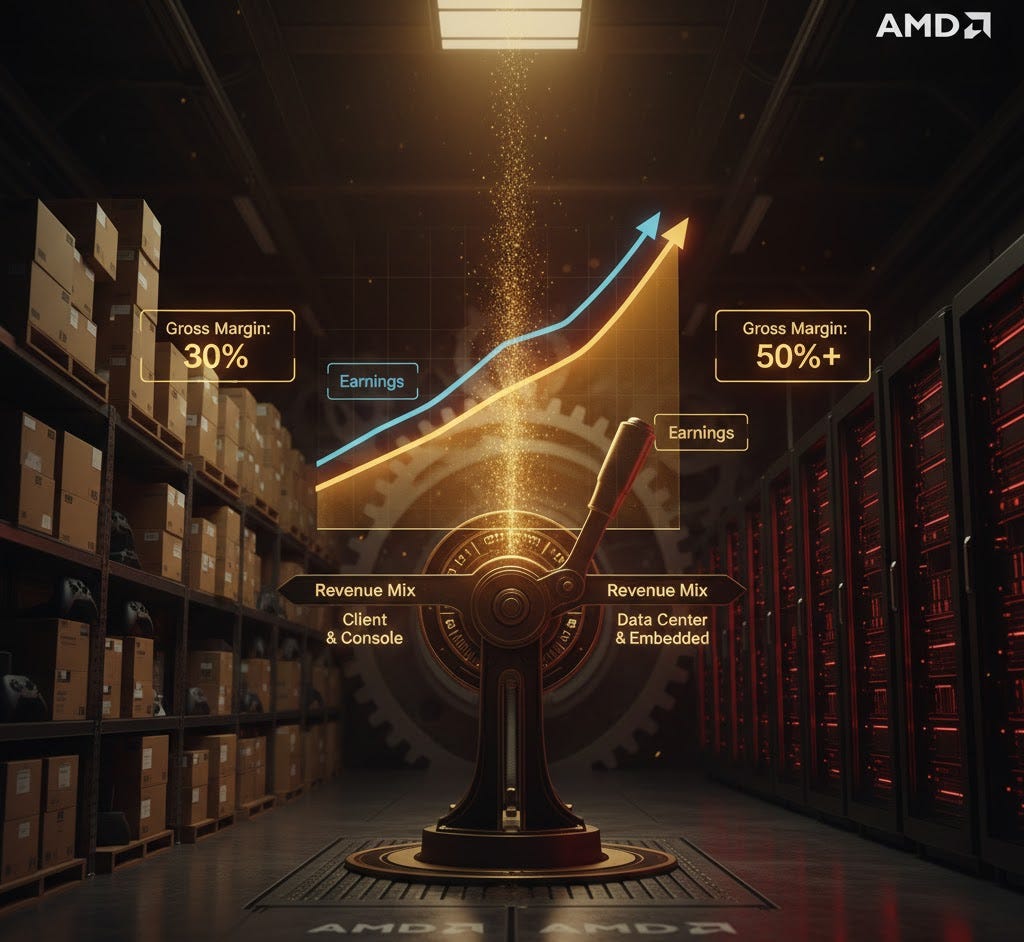

The Mix Shift: AMD is no longer just selling cheap PC chips.

Old AMD: Relied on low-margin Console and PC sales (Gross Margins in the 30% range).

New AMD: Driven by Data Center CPUs and Embedded industrial chips (Gross Margins aiming for 50%+).

The Result: As Data Center revenue overtakes Client revenue, AMD’s profitability profile improves automatically. This “mix shift” drives earnings growth faster than revenue growth.

The Competition: A Family Affair

The semiconductor industry is incestuous, but in the case of AI, it is quite literally a family matter.

The Cousin Rivalry

The Bloodline: In a twist that screenwriters would reject as too convenient, AMD CEO Dr. Lisa Su and Nvidia CEO Jensen Huang are relatives. They are first cousins, once removed.

The Context: Both trace their lineage to Tainan, Taiwan. Jensen emigrated to the U.S. as a child and Lisa followed years later. Today, they are the only two people on Earth running standalone GPU giants, controlling the engines of the AI revolution. Good genes it seems.

The Narrative

Dinner Table Diplomacy: The internet loves to imagine a weekly family dinner where Lisa and Jensen carve up the semiconductor world over dumplings.

The Reality: While they are cordial, this is a fierce, zero-sum battle for the future of computing. There is no collusion here. Nvidia wants to kill AMD’s GPU business before it can walk; AMD wants to commoditize Nvidia’s margins. They are fighting for the same trillion-dollar pie.

Nvidia (The Goliath)

The CUDA Moat: Nvidia’s advantage goes beyond its chips and extends into its software. They have a 10-year head start with CUDA, the proprietary software platform that developers use to program GPUs.

The Challenge: For AMD to win, they need more than a faster chip, which they arguably have in hardware specs; they need to convince developers to rewrite their code for AMD’s open-source platform, ROCm.

Intel (The Wounded Giant)

The Identity Crisis: Intel is trying to pull off a pivot even harder than AMD’s. They are trying to become a foundry, manufacturing chips for other companies, like Apple or even AMD, to compete with TSMC.

The Irony: If Intel succeeds in fixing its factories, it could weirdly become a partner to AMD, manufacturing Ryzen chips in Ohio. If they fail, AMD will simply continue to eat their lunch in the server market, taking share until Intel is forced to break itself up

The Moat: Chiplets & Software

AMD’s competitive advantage lies in hardware architecture, but its greatest vulnerability remains in software.

Chiplet Architecture (The Hardware Moat)

The Innovation: While Intel was still trying to manufacture massive, single-die “monolithic” chips, AMD pioneered the use of chiplets.

The Analogy: Instead of baking one giant, perfect cake, which is hard to do without burning the edges, AMD bakes several small cupcakes and frosts them together.

The Tech: Using a high-speed interconnect called Infinity Fabric, AMD “glues” smaller, cheaper dies together to act as one powerful processor.

The Economics: This approach dramatically increases yields (fewer defects per wafer) and lowers costs. It allowed AMD to offer more cores for less money, creating a price-performance gap Intel physically could not close for years.

ROCm (The Achilles’ Heel)

The Software Gap: Nvidia’s CUDA platform is the “Apple App Store” of AI; it is proprietary, polished, and sticky. AMD’s alternative, ROCm (Radeon Open Compute), has historically been categorized as the “Linux” of AI; open-source, flexible, but often buggy and difficult to use.

The Thesis Risk: AMD has the hardware to beat Nvidia (the MI300 often outperforms the H100 in raw specs), but hardware is useless without software.

The Pivot: AMD is finally treating software as a first-class citizen, acquiring startups like Nod.ai and Mipsology in 2023 to fix the user experience.

The Hope: As AI frameworks like PyTorch and OpenAI’s Triton abstract away the underlying hardware, the “CUDA Moat” is becoming shallower. If developers can code in PyTorch and run it on AMD chips without friction, Nvidia’s monopoly crumbles.

Strategic Partnerships & Alliances

AMD’s “Second Source” thesis is supported by a web of multi-billion-dollar commitments from the world’s largest tech companies, who are effectively bankrolling AMD’s R&D to ensure they have an alternative to Nvidia.

Below is a breakdown of the key alliances driving the future.

The “Anti-Nvidia” Alliance (Hyperscalers)

OpenAI (Tens of Billions): In late 2025, OpenAI and AMD announced a partnership to deploy 6 Gigawatts of compute power for future models. The deal includes warrants for OpenAI to purchase up to 160 million AMD shares, financially incentivizing the AI leader to break Nvidia’s monopoly.

Microsoft (Multi-Billion Commitment): Microsoft remains the “Anchor Tenant” for AMD’s Data Center business. They are the largest buyer of MI300X chips for Azure and continue to use AMD as the exclusive silicon provider for the Xbox Series X/S and the next-gen console roadmap.

Meta ($10B+ Est.): Mark Zuckerberg is aggressively pivoting Llama training clusters to open standards. Analysts estimate AMD captured about 40% of Meta’s GPU orders in 2025, largely displacing Nvidia for inference workloads.

Oracle (50,000 GPU Purchase): Oracle Cloud (OCI) recently announced a massive supercluster of 50,000 AMD MI450 GPUs going online in Q3 2026. As a “chip neutral” cloud provider, this massive bet validates AMD’s performance claims against Nvidia’s Blackwell.

Manufacturing & IP Partners

TSMC ($5.5B Purchase Obligations): As a fabless designer, TSMC is AMD’s lifeblood. AMD is a key launch partner for TSMC’s 2nm process and has reserved massive capacity for CoWoS advanced packaging to bypass supply bottlenecks.

Sony ($3.7B Annual Revenue): AMD is the exclusive custom chip designer for the PlayStation 5 and PS5 Pro. While cyclical, this partnership provides the reliable, high-volume cash flow that funded AMD’s survival during the lean years.

Samsung (Licensing Revenue): Samsung licenses AMD’s RDNA graphics architecture for its Exynos mobile chips. This strategic move puts Radeon graphics technology into millions of non-Apple smartphones to fight Qualcomm.

Key Strategic Acquisitions (The “M&A” War Chest)

AMD has spent heavily to fix its software weakness and build a “full stack” solution.

ZT Systems ($4.9 Billion - 2024): A direct counter to Nvidia. This acquisition allows AMD to sell entire server racks (not just chips) to Hyperscalers, significantly speeding up deployment times.

Silo AI ($665 Million - 2024): The “Software Fix.” Europe’s largest private AI lab was acquired to build custom LLMs for enterprise clients and fix the user experience on AMD’s ROCm software stack.

Nod.ai (Undisclosed - 2023): An acqui-hire of top AI compiler talent. Their technology (SHARK) helps AMD chips run open-source models (like Llama) faster than Nvidia chips.

Pensando ($1.9 Billion - 2022): The “lumbing.” Gave AMD “SmartNICs” (DPUs) to manage data flow within servers, a critical component to compete with Nvidia’s Mellanox networking division.

Xilinx ($49 Billion - 2022): The “Stabilizer.” The largest deal in AMD history expanded the company into FPGAs (aerospace, defense, industrial), providing the cash flow stability needed to survive cyclical PC crashes.

The Numbers

The financial story of AMD is a story of metamorphosis. The company has successfully shed its skin as a “cheap PC chip” manufacturer to become a high-margin Data Center titan.

Revenue Mix Shift: The “Server Flip”

For years, AMD’s fortunes rose and fell with the holiday shopping season (gaming consoles and laptops).

That era is over. In 2025, the company crossed a historic threshold where Data Center revenue officially eclipsed Client (PC) and Gaming revenue combined.

The Old AMD (2019): 70% of revenue came from PCs and Gaming.

The New AMD (2025/26):

Data Center: Now accounts for over 50% of total revenue ($16.6B+ annually), growing at 30%+ YoY.

Gaming: Has collapsed into a niche role, shrinking to <15% of the mix as the console cycle ages.

The Implication: AMD has evolved from a cyclical consumer stock to enterprise infrastructure software in hardware form.

Free Cash Flow: The “Fabless” Advantage

The most striking difference between AMD and Intel appears on the Cash Flow Statement.

Intel (The Anchor): Because Intel owns its factories, it must spend $15–20 billion annually on Capital Expenditures (CapEx) just to keep the lights on. This often pushes their Free Cash Flow (FCF) into negative territory.

AMD (The Speedboat): Because AMD outsources manufacturing to TSMC, its CapEx is negligible (often less than $1 billion).

The Result: AMD converts a massive percentage of its revenue directly into Free Cash Flow (reaching a record $2.1 billion in Q4 2025 alone). This cash is used for share buybacks and software acquisitions, not buying concrete for factories.

The “Xilinx Effect” (Embedded)

While the $49 billion price tag for Xilinx was controversial, it fixed AMD’s volatility problem.

The volatility buffer: PC and Gaming sales are erratic; they boom during holidays and bust during recessions.

The anchor: Xilinx chips go into F-35 fighter jets, 5G towers, and MRI machines. These products have 10-year lifecycles.

Proof: Even during the PC crash of 2023-2024, the Embedded segment remained cash-flow positive, preventing AMD’s earnings from going into the red. It raised the company’s floor.

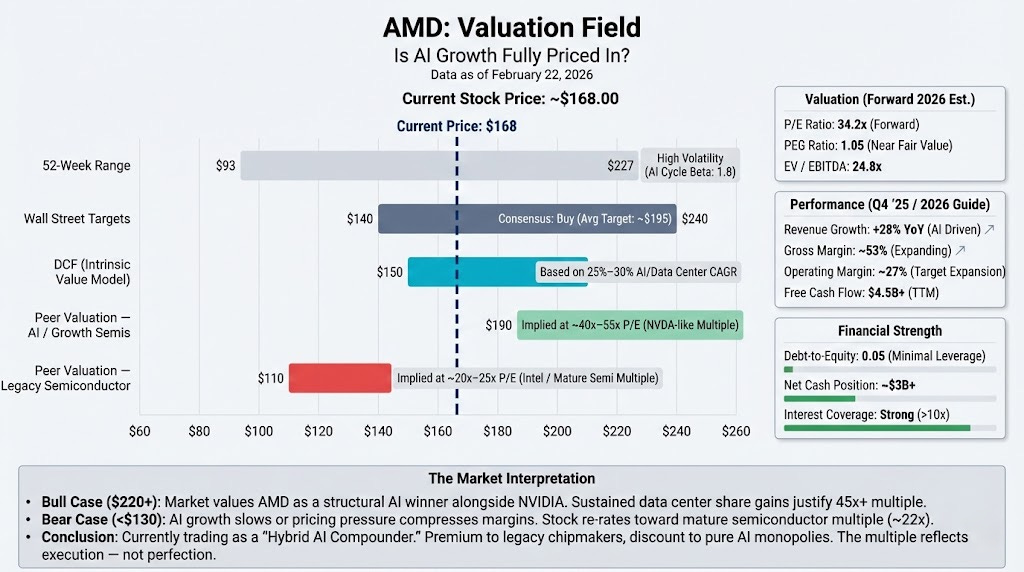

Valuation & Risks

AMD is no longer a value stock; it is a growth stock priced for a specific outcome. The market is betting that the “Second Source” thesis is inevitable.

The Valuation: The “AI Premium”

Relative Value: AMD typically trades at a discount to Nvidia on a Forward P/E basis, but at a significant premium to the broader semiconductor index and legacy peers like Intel.

The Math: The bull case rests on the Total Addressable Market (TAM). If the AI accelerator market hits $400 billion by 2027 as projected, AMD capturing just 10% market share implies $40 billion in incremental revenue.

The Question: Is the stock expensive? On trailing earnings, yes. But on 2027 earnings, if they hit that 10% target, the stock is arguably cheap. You are paying for the probability of the duopoly.

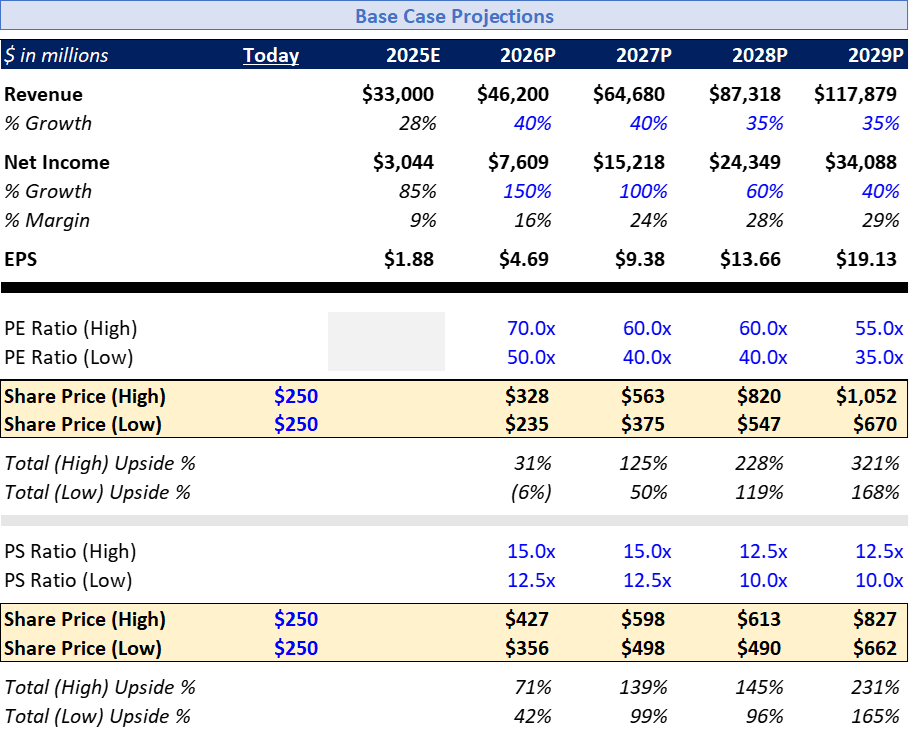

Valuation Field

Below are AMD’s financial projections base case from The Private Public Investor’s deep dive back in November 2025.

Full article here: Deep Dive on AMD (Advanced Micro Devices)

These projections show a Revenue CAGR of 37.5% and EPS CAGR of 78.6% over the next four years. If AMD can execute, the stock is poised to outperform the S&P 500 by a factor of 4x-5x.

This is the 'Blue Sky' scenario. But in the semiconductor industry, gravity is heavy and the execution tightrope is thin. You don’t get the opportunity for massive outperformance without walking through a minefield of execution risks. Let’s look at the bear case.

Risk #1: The China Disconnect

The Exposure: Historically, China has accounted for 20–25% of AMD’s revenue. It is a massive market for both their PC chips and data center products.

The Geopolitical Vise: AMD is caught in the crossfire of the U.S.-China tech war.

U.S. Bans: The U.S. government has restricted the sale of high-end AI chips, like the full-spec MI300, to China.

China’s Retaliation: Beijing has issued guidelines to phase out U.S. chips (Intel and AMD) from government servers and computers in favor of domestic alternatives like Huawei. A complete decoupling from the Chinese market would force a painful revenue reset.

Risk #2: Execution & The Supply Chain

The CoWoS Bottleneck: Designing the chip is the “easy” part; building it is much more difficult. Both AMD and Nvidia rely on TSMC for manufacturing, specifically for CoWoS (Chip-on-Wafer-on-Substrate) advanced packaging.

The Squeeze: TSMC’s capacity is finite. If Apple and Nvidia book all the advanced packaging capacity, AMD cannot ship its MI300 chips, regardless of how much demand there is. AMD must fight for allocation at the table of giants.

Risk #3: The Raw Material War (Rare Earths)

The Input Crisis: The semiconductor supply chain is incredibly fragile at the raw material level.

Gallium & Germanium: These rare metals are critical for high-speed chip manufacturing. China controls 90%+ of the global supply and refining of these elements.

The Threat: As geopolitical tensions rise, China has already begun restricting exports of these metals.

The Impact: A supply shock would lead to skyrocketing input costs or, worse, production halts. While AMD is fabless and doesn’t buy these metals directly, their partners (TSMC) do. Any cost spikes will be passed directly to AMD, threatening the gross margin expansion narrative that investors are banking on.

Final Thoughts

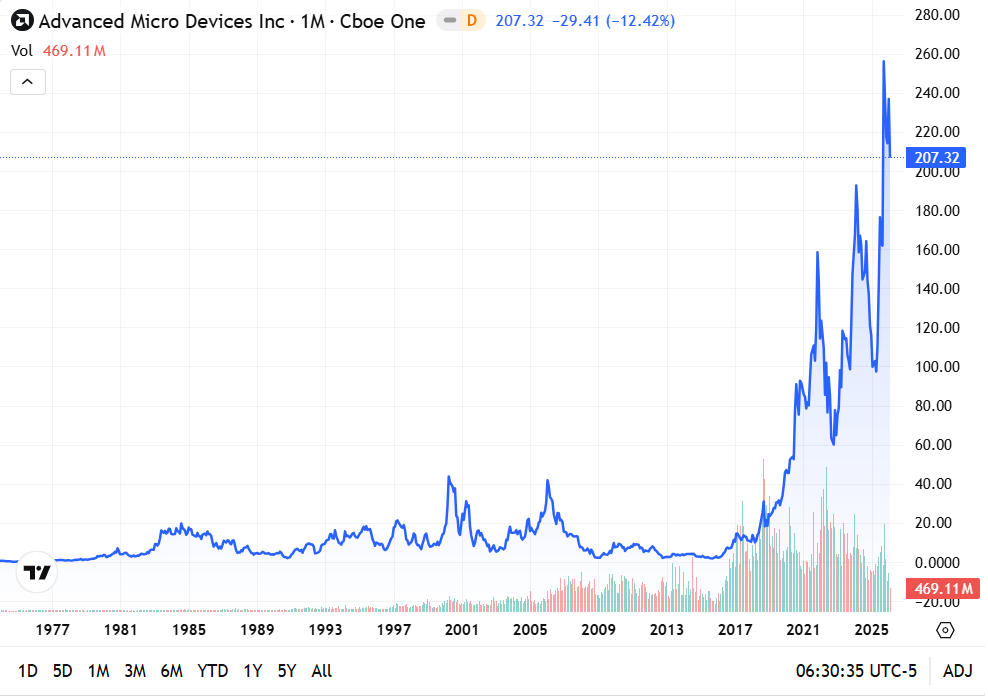

For fifty years, AMD was defined by what it wasn’t: It wasn’t Intel. It was the budget option, the generic brand, the “good enough” chip for students and budget gamers.

That era is dead. Today, AMD is a premium technology leader; they surpassed Intel’s market cap in February of 2022 and never looked back.

The Valuation Reality: The stock is no longer cheap, but neither is the opportunity. The investment thesis does not require AMD to dethrone Nvidia. It simply requires the market to demand an alternative.

The Math: The AI accelerator market is projected to hit $400 billion by 2027.

The Bull Case: If AMD captures just 10–20% of this market as the “Second Source,” they will generate more revenue from AI alone than they did as an entire company in 2022. In a market of this scale, being the clear #2 is a trillion-dollar opportunity.

The story of AMD is the greatest turnaround in the history of the semiconductor industry.

It began with Jerry Sanders, a salesman in a white suit who shouted that “real men have fabs” while fighting for scraps. It concludes with Dr. Lisa Su, an engineer who quietly sold the fabs, fixed the chips, and now stands toe-to-toe with her leather-jacket-wearing cousin, Jensen Huang.

The “uninvestable” stock that traded at $1.61 in 2015 has evolved into the backbone of the modern data center. The Empire didn’t just strike back; it built a better Death Star.

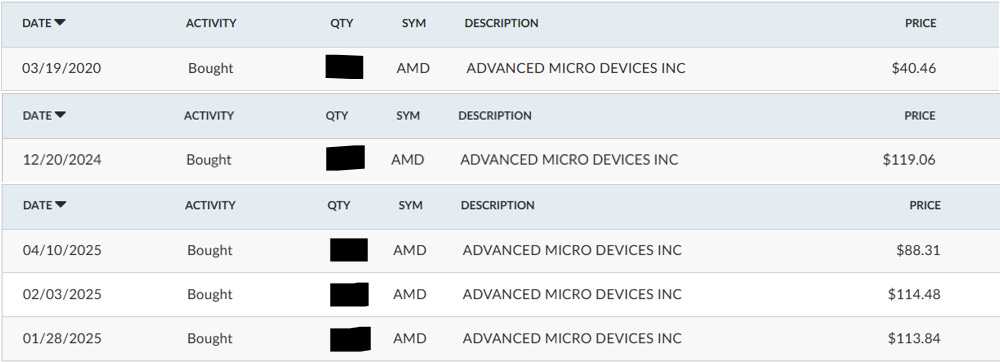

Receipts: Putting My Money Where My Mouth Is

As always, I have included receipts for all my purchases while hiding the quantity of shares and my account number for privacy.

My current position is at an average price per share of $75.06.

Disclaimer:

I’m not your financial advisor, your lawyer, or your life coach (though I do wish you well). This content is for informational and entertainment purposes only. It is not financial advice, and it should not be treated as such. Investing involves risk, including the risk of losing your money, your patience, and possibly your hair. Always do your own research, consult with licensed professionals, and never invest more than you can afford to lose.

Good work, but I find your base case overly optimistic.